How Buy-and-Build Strategy Works in Fragmented European SME Markets

A buy-and-build strategy acquires one well-chosen company, the platform, and uses it as the operational foundation for a sequence of add-on acquisitions in the same fragmented sector. The platform contributes existing customer relationships, technical credibility, and management infrastructure. Each add-on acquisition expands geographic reach or service capacity while sharing central costs across a growing group. The value creation logic is structural: a €1 million EBITDA business acquired at a small-company multiple is worth materially more when it anchors a consolidated group with a diversified customer base, proven leadership, and demonstrable scale. According to the Dealsuite European M&A Monitor (H2-2024), businesses generating €200,000 in EBITDA trade at approximately 3.9x, while businesses generating €10 million in EBITDA trade at 7.2x. That gap between the small end of the market and the mid-market reflects a real risk premium, and buy-and-build exists to earn it away through operational work. WAD Capital executes this model across fragmented Belgian and Dutch sectors including HVAC, fire safety, and physical security through its CEO-in-Residence (CIR) programme.

What Does "Fragmented Market" Actually Mean for Acquisition?

Fragmentation gets used loosely. In buy-and-build terms, it has a specific operational meaning: a market where demand is served by dozens or hundreds of owner-operated businesses, none of which has achieved regional dominance, and where the primary barrier to consolidation is not capital or regulation but the absence of a capable, permanent operator willing to do the work.

Belgian HVAC is a useful example. Thousands of heating, ventilation, and air conditioning businesses operate across Wallonia and Flanders. The majority are founder-led, employ between ten and one hundred people, and generate stable EBITDA from residential and commercial maintenance contracts. They have loyal local customer bases built over decades. They also have no succession plan, no professional management layer below the founder, and no path to the kind of scale that would make them attractive to a larger acquirer. The market is not broken. The businesses are sound. The structure is atomised.

That atomisation is precisely what makes fragmented markets attractive for buy-and-build. Entry multiples stay compressed because buyers are scarce and institutional capital rarely operates at this scale. Operational improvements compound quickly because the starting point is often a business that has never had a dedicated finance function, a formal CRM, or a systematic approach to key account management. The exit case, a regional leader with proven management, diversified revenue, and documented financials, is a materially different asset from the platform company that started the process.

The 2024/2025 European Commission SME Performance Review estimates that approximately 690,000 SMEs across the EU face ownership transition each year. The sectors most heavily represented are manufacturing, construction, and B2B services: the same sectors that tend toward fragmentation, founder-dependency, and structural underinvestment in management. Not all of them are right for buy-and-build. Identifying the ones that are is where the work starts.

How to Identify the Right Platform Company

A platform acquisition is not simply the first company a CIR finds. It is the company that can credibly anchor a group, one whose operational foundations are strong enough to absorb management attention from add-on integrations without losing ground in its core business.

Three criteria matter above all others when evaluating a platform candidate in a fragmented market.

The first is technical credibility in the sector. An HVAC consolidation platform needs certified engineers, AGR-Gaz credentials, and a track record with both public and private sector clients. A physical security platform needs decades of installation history and a customer base that trusts the firm with access control and intrusion detection. These credentials cannot be acquired quickly. They accumulate slowly, and they transfer through acquisition, which is why buying an operationally excellent smaller company beats buying a larger but technically weaker one.

The second is a customer base with genuine stickiness. Service businesses in fragmented sectors often have renewal dynamics that look nothing like contract-based SaaS but function similarly in practice. An HVAC maintenance customer who has used the same provider for fifteen years and whose boiler the engineer knows by serial number is not actively shopping around. That relationship has real value. It should be documented, understood, and protected during the transition.

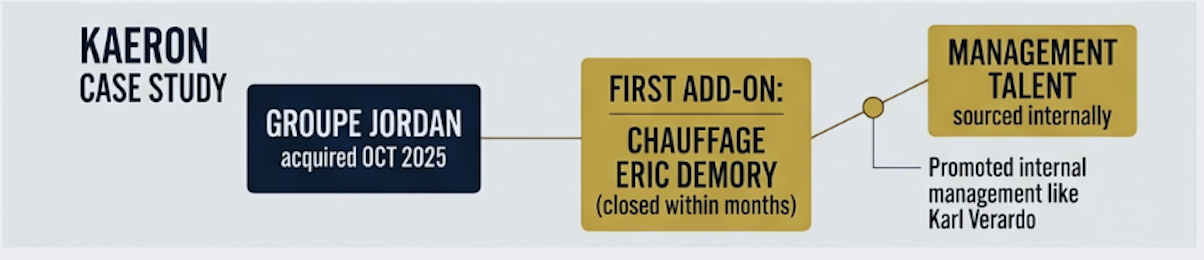

The third is founder continuity where available. When Frédéric Schilling acquired Groupe Jordan in Farciennes, Hainaut, in October 2025, the founding acquisition of Kaeron, Jean-Luc Stavaux did not simply hand over the keys and leave. He reinvested and remained involved as Sales and Marketing Director. That decision preserved customer relationships built over years and gave the incoming team access to sector knowledge that would have taken months to reconstruct from scratch. Post-acquisition continuity of this kind is not guaranteed. When it is achievable, it substantially reduces execution risk in the first twelve months.

What the Add-On Acquisition Logic Looks Like in Practice

The Kaeron platform illustrates the sequencing. Groupe Jordan gave Frédéric Schilling a foundation: 110 employees, certified technicians, a public and private sector client base across Hainaut, and a profitable HVAC maintenance and installation operation. From that base, the add-on thesis is straightforward. Identify adjacent HVAC operators within the Benelux, acquire them at off-market entry prices, integrate them operationally under the Kaeron group structure, and expand the combined entity's geographic reach without duplicating management overhead.

Kaeron's first follow-on acquisition, Chauffage Eric Demory in Brussels, was sourced and led by Karl Verardo, a manager developed from within the Groupe Jordan team. In a successful buy-and-build, the platform does not just provide a customer base. It develops the management talent that leads subsequent acquisitions. The group compounds human capital alongside financial capital.

OmniSecur, WAD Capital's physical security platform built around Alsec SA in Nivelles, applies the same logic to a different sector. Steven Bourgeois acquired Alsec, a Wallonia-based physical security installer founded in 1987, in November 2025. The thesis was explicit from the start: acquire the technical prime player in a fragmented market first, establish credibility and operational standards, then add high-margin security installers with existing B2B customer bases. The sector tailwind is structural. Tightening fire safety and security compliance regulation across Belgium creates predictable demand for professional, accredited installers, exactly the profile that a consolidated group can serve at scale where individual owner-operated firms cannot.

Both platforms share the same entry logic: buy the most technically credible operator in the subsector, not necessarily the largest, and use that technical credibility to lead the consolidation rather than following it.

Why SME Consolidation Strategy Fails Without the Right Operator

Buy-and-build is not primarily a financial strategy. It is an operational one that happens to produce financial returns. The majority of SME consolidation attempts that stall do so not because the capital was wrong or the market was insufficiently fragmented, but because the person running the platform company was not equipped for the specific demands of simultaneous integration and organic operation.

Running an acquired SME in year one already requires navigating a new management team, a founder's residual influence, a customer base that is watching closely for signs of change, and a set of operational processes that exist mostly in people's heads rather than documented systems. Add an active acquisition process for add-ons, and the demands on a single operator become significant. Managing deal flow, conducting due diligence, negotiating terms, and coordinating financing while running day-to-day operations is not a theoretical challenge. It is what the job actually looks like.

WAD Capital's cohort model addresses this directly. CIRs searching for acquisitions across adjacent sectors share pattern recognition in real time. The executive who acquired a fire safety business six months ago has already encountered the integration challenges that the CIR closing an HVAC deal this month will face in twelve weeks. That accumulated operational knowledge, covering what the first thirty days of team communication should look like, which financial reporting changes to make immediately versus which to defer, and how to sequence the conversation with the seller's longest-serving employees, is not available to a solo searcher building a buy-and-build from scratch.

WAD Capital Fund I, a Belgian privak (pricaf privée) regulated by the FSMA, provides 100% of acquisition financing. No personal capital investment is required from the CEO-in-Residence. The CIR is not financing the platform acquisition from personal resources, which means the capital available for add-on acquisitions is not constrained by the platform CEO's personal balance sheet. The institutional base scales with the strategy.

What Fragmented Market Multiples Mean for Value Creation

The Dealsuite European M&A Monitor (H2-2024) documents the multiple compression at the small end of the market with precision. At €200,000 EBITDA, the average European acquisition multiple is approximately 3.9x. At €10 million EBITDA, it is 7.2x. The gap reflects the risk premium buyers apply to smaller, founder-dependent, structurally under-managed businesses. Buy-and-build exists to earn that premium away through operational work, not financial engineering.

A platform company grown through several add-on acquisitions, with documented management, diversified customer revenue, and a clean operating structure, is no longer a small-company asset. It is an asset that a mid-market private equity firm running a sector consolidation strategy, or a strategic acquirer seeking regional presence, will price at the larger end of the market range. That is the exit case. It does not require a miraculous operational transformation of any individual business. It requires competent management, time, and the patience to integrate carefully rather than quickly.

WAD Capital's typical holding period is 5–7 years across its portfolio. That timeline is calibrated to the buy-and-build cycle: enough time for a platform to absorb multiple add-on acquisitions, for management systems to mature, and for the consolidated entity to generate several years of audited financials as a group, which is what the eventual buyer will require before pricing at the upper end of the market range.

The 32% of European sell-side assignments discontinued before completion, per the Dealsuite European M&A Monitor (H2-2024), are disproportionately concentrated among businesses that come to market without institutional-quality documentation, with a single founder-dependent revenue stream, or with management that cannot demonstrate continuity post-sale. A well-executed buy-and-build produces the opposite profile.

How WAD Capital Identifies Fragmented Sectors for Buy-and-Build

CIRs entering WAD Capital's programme do not begin with a target company. They begin with a sector thesis. The first phase of the 12-step acquisition programme is dedicated to Investment Memo Creation: deep market analysis, expert interviews to stress-test the thesis, and a structured assessment of whether the sector exhibits the fragmentation characteristics that make buy-and-build viable. Concentrated demand, no dominant regional operator, owner-operated businesses with stable cash flows and genuine succession pressure.

During the Market Mapping phase, CIRs build a comprehensive picture of a subsector across the Benelux: who is operating, who is approaching retirement age, which operators have the technical credentials that would make them viable platform anchors, and where sub-sector geography creates natural consolidation logic. Using Generative DealFlow™, WAD Capital's proprietary deal-sourcing methodology, the firm screens acquisition candidates continuously across the target market and identifies targets that are not listed on any broker's mandate. The majority of WAD Capital's deal flow is sourced through direct, off-market engagement rather than competitive processes.

By the time a CIR reaches the Letter of Intent stage of the programme, they have had structured conversations with a substantial number of business owners, built genuine relationships with the most promising candidates, and developed a sector understanding that a solo searcher would take a year or more to accumulate. That upfront investment in thesis and market knowledge is what produces off-market entry in sectors with structural demand tailwinds.

Is a Buy-and-Build Strategy Right for Your Sector?

Not every fragmented sector supports a buy-and-build strategy. The ones that do tend to share a small number of characteristics: recurring or structurally non-discretionary demand, services that require local physical presence, technical credentials that accumulate over time rather than being easily replicated, and a customer base that values relationships and continuity over pure price competition.

HVAC maintenance, fire safety compliance, physical security installation, electrical works, and waste management all fit that profile. Industrial manufacturing, specialist logistics, and healthcare services in specific sub-sectors often do too. Generic professional services such as legal, accounting, and generalist consulting typically do not. The fragmentation is real in those markets, but switching costs are lower, customer relationships are thinner, and technical differentiation between operators is harder to establish and defend.

For a CIR evaluating whether their sector thesis supports a buy-and-build, the diagnostic questions are concrete. Can you map a large universe of owner-operated businesses within the Benelux that generate stable EBITDA in this sector? Are a significant proportion of those owners approaching retirement with no succession plan in place? Does technical credibility in the sector compound with time in ways that create durable customer stickiness? Is there no currently dominant regional consolidator? If the answers are yes, the sector warrants serious investigation.

WAD Capital's 2026 cohort is now recruiting. Applications are open at wadcap.com/join-cir.