What Is Entrepreneurship Through Acquisition and Is It Right for Europe?

Entrepreneurship Through Acquisition (ETA*) is a model in which an experienced executive acquires an existing, profitable business rather than building one from scratch or joining a startup. The acquirer — typically with 10 to 20 years of operational experience — identifies a target company, secures financing, negotiates and closes the acquisition, then steps in as CEO with an equity stake. In the United States, the model has been documented since the 1980s. The 2024 Stanford GSB Search Fund Study records a 35.1% aggregate pre-tax IRR across 681 funds. In Europe, the model is earlier stage: the 2024 IESE International Search Fund Study tracks 320 international search funds, with 85 acquisitions completed across the continent. WAD Capital operates an institutional variant of ETA* in Belgium and the Benelux, running cohorts of approximately ten CEO-in-Residence (CIR) candidates simultaneously, each fully financed by WAD Capital Fund I, a Belgian privak regulated by the FSMA.

What Does Entrepreneurship Through Acquisition Actually Mean?

The name is precise. You acquire a business. You run it. The entrepreneurship is in the ownership and the operational leadership, not in the invention of a product or the building of a customer base from zero.

This matters because the risk profile is fundamentally different from starting a company. The business you acquire already has revenue, customers, employees, and an operational history. The succession problem you are solving — a founder who has spent 25 or 30 years building something and has no natural successor — is not a sign of business weakness. In the SME segment that ETA* targets, the most common reason a profitable, well-run company comes to market is that its owner is retiring, not that the business is deteriorating. You are stepping into an operating engine. Your job is to keep it running and then improve it.

The alternative paths to business ownership are worth naming briefly, because ETA* is often misunderstood by comparison to them. Starting a company from scratch gives you full control and zero revenue on day one. Buying a franchise gives you a proven system and limited autonomy. An MBO requires the management team to buy out the existing owner, which demands personal capital and negotiating across a relationship. ETA* is a different instrument: you identify a business you want to lead, you bring institutional backing to the acquisition, and you become its owner-operator with meaningful equity from the outset.

Where Did the ETA Model Come From and Why Did It Start in the US?

The search fund model was first documented at Harvard Business School in 1984 and developed at Stanford GSB through the 1990s and 2000s. The original structure was simple: an entrepreneur raises a small amount of capital from a group of investors to fund a search for a company to acquire. Once a target is identified, the same investors (typically) provide the acquisition financing. The entrepreneur becomes CEO with a significant equity stake.

The US conditions that made this viable were specific. A large, fragmented SME market. A well-developed community of individual investors familiar with the model. MBA programmes that trained searchers in deal mechanics. A legal and financial infrastructure built for transaction execution by individuals without institutional backing.

Europe had the SME market but not the ecosystem. Individual search funds in Europe began appearing in meaningful numbers only around 2015, according to IESE's tracking data. The legal complexity of acquiring across multiple jurisdictions, the language fragmentation, and the absence of a trained investor community slowed adoption. The model that worked efficiently for a Stanford MBA acquiring a plumbing supplies company in Texas did not transfer cleanly to a Brussels-based executive pursuing an HVAC business in Hainaut.

What changed is that institutional platforms entered. Rather than each searcher building their own infrastructure, financing relationships, and deal sourcing capability from scratch, structured programmes began providing those elements centrally.

Why Is ETA a Different Path to Business Ownership Than Starting a Company?

Three things distinguish ETA* from conventional entrepreneurship in ways that matter to an experienced executive evaluating the model.

First, the starting point. An acquired business has a track record. You can read three years of management accounts, understand customer concentration, assess employee tenure, and evaluate margin structure before committing. The uncertainty that kills early-stage startups — whether anyone wants the product, whether the unit economics work, whether the team can execute — is largely resolved. You are making a bet on operational improvement, not on existence.

Second, the capital structure. Institutional ETA* removes the personal capital requirement that stops most executives from pursuing acquisition independently. WAD Capital provides 100% of acquisition financing. No personal investment is required from the CEO-in-Residence, though co-investment is encouraged for alignment. The searcher receives a monthly management fee during the search phase, a competitive CEO salary post-acquisition, and an equity stake of up to 20% vesting across three value-creation milestones. The financial exposure most executives assume is inherent in business ownership turns out to be a feature of self-funded search, not of the model itself.

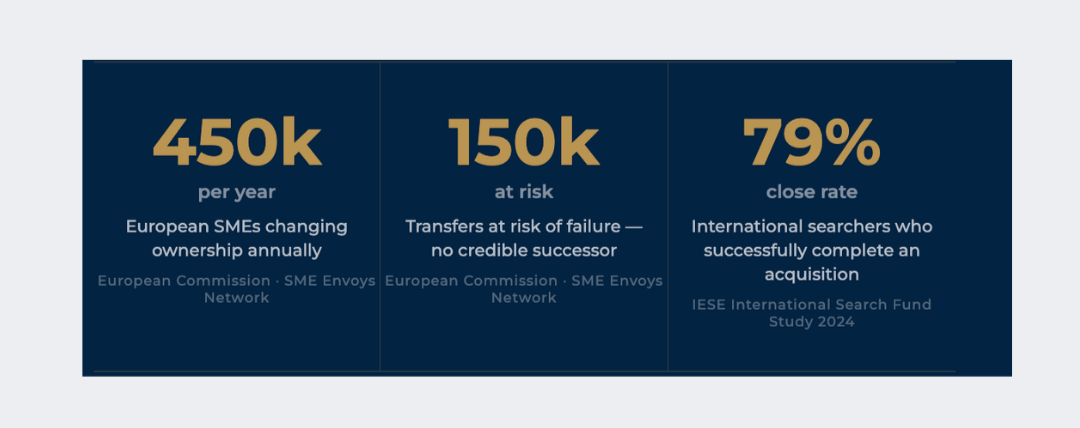

Third, the selection dynamic on the other side of the table. A retiring founder is not choosing between five institutional bidders in an auction. They are choosing between a small number of potential successors, and they are choosing as much on character and continuity as on price. The 2024 IESE International Search Fund Study found that 79% of international search fund entrepreneurs had successfully acquired companies by the end of 2023. Acquisition rates that high reflect a market where the supply of transferable businesses is large and the competition for them is thin relative to what most executives assume.

How Many European SMEs Are Available for Acquisition Right Now?

The supply side of ETA* in Europe is not a bottleneck. According to the European Commission Network of SME Envoys, approximately 450,000 European SMEs change ownership annually, with roughly 150,000 of those transfers at risk of failure. These are businesses that have operated for decades, employ real people, serve established customer bases, and face one specific problem: their founders are retiring with no credible succession plan.

The KfW Nachfolge-Monitoring Mittelstand study found that 230,000 German SMEs needed a new owner in 2024 alone, with approximately 125,000 successions required per year through 2027. Germany is one market. Add the Netherlands, Belgium, France, and adjacent Benelux territories and the addressable supply within 300 kilometres of Brussels is substantial.

What this means practically is that ETA* in Europe is a buyer's market in a specific sense: the founders who most need successors are not optimising for the highest multiple. They are optimising for the right person. An executive who can demonstrate sector credibility, genuine interest in preserving what the founder built, and the backing of an institutional fund is a more compelling counterparty to a retiring 65-year-old Belgian business owner than a financial consolidator offering a marginally higher price.

Frédéric Schilling understood this when he acquired Groupe Jordan, a Hainaut-based HVAC business with approximately 110 employees, through WAD Capital in October 2025. The company's founder, Jean-Luc Stavaux, reinvested in the business and stayed on post-acquisition. That kind of outcome happens when the acquirer is the right person, not just the highest bid.

The full demographic picture behind that number, country by country, with the data on where the successor gap is widest, is broken down separately: https://wadcap.com/blog/the-european-succession-crisis-in-numbers-what-the-data-actually-shows

What Does the Data Say About ETA Returns in Europe vs. the United States?

The honest answer involves reading two datasets in sequence rather than picking the one that suits a given argument.

The 2024 Stanford GSB Search Fund Study records a 35.1% aggregate pre-tax IRR and 4.5x ROI across 681 search funds formed in the US and Canada since 1984. That figure has held remarkably stable across three successive biennial studies. It reflects a mature market with three decades of exits, a trained investor community, and a cohort of searchers who came up through a well-developed institutional pipeline. The 2017–2020 acquisition cohort within the Stanford data shows IRR trajectories above 50% for funds that have had sufficient time to compound.

The 2024 IESE International Search Fund Study records 18.1% IRR and 2.0x ROI for international search funds across 40 countries outside North America. That gap is real. It is also almost entirely explained by timing. The IESE study notes that 62% of all international acquisitions have occurred since 2020, meaning the majority of those companies have had fewer than four years to compound returns that the Stanford data shows are heavily back-loaded. Early European cohorts are sitting at the same point on the return curve that early US cohorts occupied in the mid-1990s.

Treat the Stanford figure as the mature-market proof of concept. Treat the IESE gap as where European ETA* currently sits in a maturation cycle, not where it is heading.

What Is the Difference Between a Traditional Search Fund and an Institutional ETA Programme?

A traditional search fund is a solo venture. One searcher raises capital from a small group of individual investors, typically 10 to 15 people, to fund 18 to 24 months of deal sourcing. The searcher builds their own pipeline, writes their own outreach, negotiates their own diligence workstreams, and goes back to the same investors for acquisition financing once a target is identified. The infrastructure for every part of that process is built from scratch, on the clock, while the search capital depletes.

The 2024 Stanford study shows the median acquisition takes 20 months. Four in ten searchers never close a deal at all. The model works when it works — the return data is real — but the failure rate and timeline reflect structural features of the solo approach that are not inherent to ETA* as a concept.

An institutional ETA* programme changes the architecture. 99% of WAD Capital's deal flow is sourced through Generative DealFlow™, the firm's proprietary AI-powered sourcing mechanism, and direct CIR outreach. This produces off-market acquisitions at sub-5x EBITDA multiples, compared to 12–15x in competitive auction processes. A CEO-in-Residence joining the programme on day one has login credentials to a Deal Intelligence Platform with tens of thousands of companies already screened and filtered, legal and financial templates tested across completed acquisitions, and a 12-step acquisition programme with defined timelines, KPIs, and investment committee checkpoints at each stage.

The difference is not marginal. A solo searcher in month three is still choosing a CRM. A WAD Capital CIR in month three is reviewing a shortlist of target companies in their chosen sector.

How Does WAD Capital's CEO-in-Residence Programme Adapt ETA* for the Benelux?

WAD Capital is Europe's only institutional search fund. The CEO-in-Residence Programme is a 12-to-24-month structured acquisition process in which experienced executives join a cohort of approximately ten candidates, source their own SME acquisition using WAD's proprietary infrastructure, negotiate and close the deal, then become CEO of the acquired business with an equity stake.

The European adaptations are specific. The geographic focus within approximately 300 kilometres of Brussels matches the relationship-driven nature of Belgian and Dutch SME succession: sellers in these markets do not typically run competitive auctions. They transfer businesses to people they trust. Direct, CIR-led outreach — grounded in genuine sector expertise and supported by WAD's deal sourcing technology — fits that dynamic better than a broker-intermediated process.

The cohort model is a second adaptation. Rather than isolating each searcher as an individual, WAD Capital runs approximately ten CEO-in-Residence candidates simultaneously. They share pattern recognition across sectors, compare notes on outreach responses, and draw on a common operational infrastructure. Someone six months ahead in the search process has already solved problems the next CIR is encountering for the first time. That institutional learning circulates in near real time.

WAD Capital evaluates more than 500 candidates per cohort and selects approximately ten. The 50:1 ratio is not a credential filter. It is the mechanism by which the cohort contains the operator profiles that ETA* data consistently associates with strong outcomes: deep sector expertise, demonstrated P&L accountability, and a credible right to win in a specific fragmented market. Applications for Cohort 2026 are open at /join-cir. Programme mechanics are detailed at /faqs/ceo-in-residence.

Is Entrepreneurship Through Acquisition Right for You?

The model suits a specific profile. Not every accomplished executive is the right candidate, and being honest about that is more useful than a broad recruitment pitch.

ETA* works for executives who have genuine sector depth — not just adjacent familiarity, but the kind of knowledge that lets you evaluate a target company's customer relationships, operational structure, and competitive position from the inside. The investment thesis you build in the first weeks of the programme is the intellectual foundation for everything that follows. If it lacks credibility, no amount of sourcing effort will compensate.

It works for people who want to run a business, not manage one. The CEO of a 50-person Belgian HVAC company is in the operations on Monday morning, not in a strategy offsite. The distance between corporate execution and owner-operator accountability is real, and candidates who underestimate it tend to struggle in the first months post-acquisition.

It is not the right path for executives who need a short commitment horizon, who are not prepared to work full-time across the search phase, or who are primarily motivated by financial upside without genuine interest in the sectors and businesses they would be acquiring.

The businesses available through ETA* in Europe are genuinely worth preserving. They represent decades of accumulated relationships, operational knowledge, and community trust. The executives who acquire them well are the ones who understand that before they understand the exit multiple.