The European Succession Crisis in Numbers: What the Data Actually Shows

The European Commission estimates that 690,000 SMEs and 2.8 million jobs are affected by ownership transfers each year across the EU. Roughly a third of those transfers are at risk of failure. Not because the businesses are weak, but because there is no one to take them over.

SMEs account for 99.8% of all enterprises in the EU, according to the European Commission's 2024/2025 SME Performance Review. Eurostat's 2024 data counts roughly 33.5 million enterprises across the EU employing 164.2 million people, with SMEs contributing 51.4% of value added in the non-financial business economy. When we talk about the succession crisis, we are talking about the operating system of the European economy. And that system is running into a demographic wall.

The Continental Picture

One third of EU business owners will retire over the next decade (European Commission). That single statistic underpins everything that follows. The baby boom generation that built Europe's SME base is leaving, and the generation behind it is smaller, differently educated, and less inclined toward business ownership.

The data is most granular in Germany, where KfW Research has been tracking succession since 2015. Their January 2025 report found that 231,000 German SME owners were considering closing their businesses by the end of 2025, a 41% increase over the prior year and the highest figure ever recorded (KfW Nachfolge-Monitoring Mittelstand 2024). Across Germany's 3.84 million SMEs, 39% of owners are already over 60. The average owner age is 54. By 2028, 532,000 German SMEs intend to find successors, while a roughly equal number are considering closure instead.

France faces 700,000 company transitions in the next decade. In the Netherlands and Belgium, the same demographic wave is building across a combined SME base of over 1.1 million enterprises. Belgian SMEs employ 66.3% of the country's workforce, higher than in France, the Netherlands, or the EU average (European Commission, SME Performance Review). When these businesses fail to transfer, the impact is concentrated directly in local employment.

Where the Successor Gap Comes From

Across Europe, the supply of people willing and able to take over existing businesses is structurally insufficient. KfW's data shows that each year there are fewer than half as many business takeovers as there are SMEs with active succession plans (KfW Status Report on SME Succession, 2024). The DIHK (German Chambers of Industry and Commerce) quantifies the gap differently but reaches the same conclusion: for every individual who contacts a chamber of commerce interested in acquiring a business, more than three businesses are already there looking for a buyer. That ratio has been widening consistently since 2012 (DIHK Report on Company Succession, 2023).Seventy-four per cent of businesses cite finding a suitable successor as their primary hurdle, according to KfW. Purchase price disagreement comes in at 30%, bureaucracy at 30%, legal complexity at 28%, and financing at 16%. The successor shortage dominates by a wide margin. Family succession remains the preferred option for 57% of owners. But the main reason owners cite for planned closures is lack of interest from family members, at 63%, up 13 percentage points from the prior year's KfW report. Younger generations are pursuing corporate careers, tech roles, and consulting tracks. Running a 40-person industrial services firm in Charleroi or Eindhoven is not competing effectively for that talent pool.

External succession solves the family pipeline problem in theory. In practice, a potential buyer needs capital, needs operational credibility in the relevant sector, needs to earn the trust of a founder who built something over thirty years, and needs to close a transaction in a market where information asymmetry runs deep. Most people who would make excellent owner-operators of a €2M EBITDA business have no mechanism to find, evaluate, finance, and acquire one.

For more information visit our FAQs page wadcap.com/faq

What This Looks Like at Transaction Level

Dealsuite's European M&A Monitor (H2-2024) provides the clearest view of what actually happens when SMEs come to market. The average European EBITDA multiple sits at 5.25, but that average obscures enormous variation by company size. Businesses generating €200,000 in EBITDA trade at approximately 3.9x. Businesses generating €10 million in EBITDA trade at 7.2x. The gap is 3.3 turns of EBITDA (Dealsuite European M&A Monitor, March 2025).

Smaller companies carry higher risk premiums, attract fewer institutional buyers, and receive less advisory attention. These are precisely the businesses where succession is most acute.

Not every sale mandate reaches a successful close. Dealsuite reports that 32% of sell-side assignments across Europe are discontinued before completion. The primary cause is unrealistic valuation expectations from the seller. Regional variation is significant: the Netherlands has a relatively high close rate of 78%, compared to 62% in the DACH region and 59% in CEE (Dealsuite, H2-2024). Emotional factors compound the structural ones. Twenty-nine per cent of owners seeking advice from chambers of commerce struggle to let go, and 20% delay hoping for a higher future price.

The Benelux Up Close

Belgium has approximately 717,000 SMEs in non-financial business sectors (European Commission, 2023 data), with over half located in Flanders. The Netherlands adds roughly 450,000 SMEs. Together, these economies represent a dense concentration of owner-managed businesses where generational transfer is accelerating.

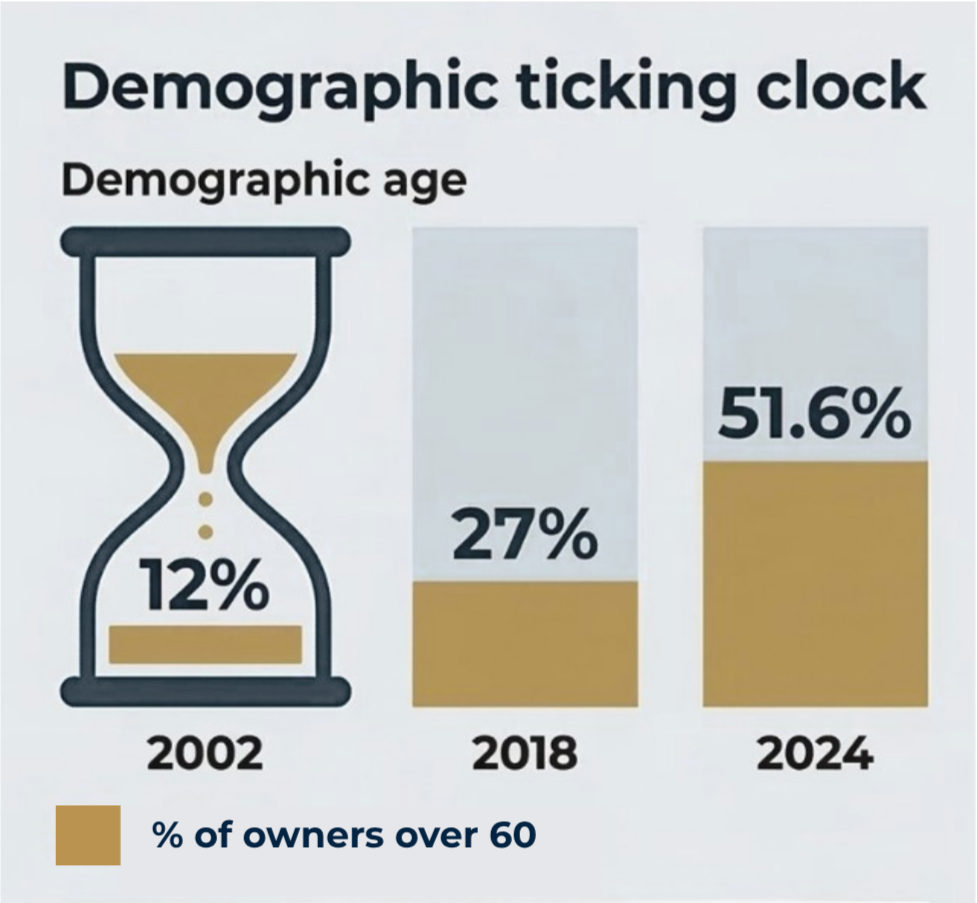

WAD Capital's own demographic analysis tracks the ageing of Belgian SME ownership: the share of SME owners over 60 rose from 12% in 2002 to 27% by 2018, with projections reaching 51.6% by 2024. Only 18% of Belgian SME managing directors are women, one of the lowest rates in Western Europe, which further narrows the already thin pipeline of potential successors.

The Benelux has stronger institutional investor infrastructure than many other European markets, and the Netherlands' high sell-side close rate suggests a somewhat more efficient transfer ecosystem. But the fundamental arithmetic is the same across the region: more businesses need new ownership than there are qualified buyers to acquire them.

Consider the practical mechanics. An SME owner in Wallonia runs a €3M revenue industrial services business, €800K EBITDA, 25 employees. The founder is 63. No children interested in taking over. At a 4x multiple, the business is worth roughly €3.2M in enterprise value. The local M&A broker has three similar mandates and limited bandwidth. The business is too small for mid-market private equity, too complex for a solo buyer without industry experience, and too illiquid for a standard financial transaction. The founder knows the business is good, knows the employees depend on it, and has no mechanism to connect with someone qualified to run it.

Multiply that scenario by tens of thousands across Belgium, the Netherlands, and northern France, and you have the succession crisis in operational terms.

What a Structural Response Requires

The data points toward a specific market failure: there are more good businesses available than there are qualified, capitalised operators to acquire them. Fixing this requires addressing both sides of the equation simultaneously. Operators need capital, deal flow, diligence infrastructure, and a search process that does not require spending 18 to 24 months burning personal savings before identifying a target.

WAD Capital's CEO-in-Residence programme is built as a direct response to this structural gap. Selected executives enter a 12-month search backed by full acquisition financing, proprietary deal sourcing technology that screens thousands of SMEs within approximately 300 kilometres of Brussels, and operational support covering legal, financial, and technical due diligence. The programme evaluates over 500 candidates annually and selects approximately 10 per cohort, each developing a sector thesis aligned with a specific vertical where succession activity is concentrated.

The target acquisition range of €1-5M EBITDA maps directly to the segment where the succession crisis is most acute and institutional attention is thinnest. The ownership structure, 80% fund and 20% operator equity vested across value creation milestones, aligns incentives over the long term rather than optimising for a quick exit.

Thirteen CEOs-in-Residence are currently active across sectors from pharmaceutical manufacturing to transportation logistics to fire safety, operating in the Benelux and surrounding regions. Each represents a data point in what is ultimately a supply-side intervention: putting qualified, capitalised operators into businesses that the market is otherwise failing to match with successors.

Europe's demographic trajectory is fixed for the next two decades. The succession wave will not wait for better policy frameworks or more favourable market conditions. The question is whether enough structured capital and operational talent can reach the €1-5M EBITDA band before hundreds of thousands of viable businesses simply close.

The model that supply-side response actually looks like, where it came from, what the returns data shows, and why Europe is where it goes next, is explained here: https://wadcap.com/blog/what-is-entrepreneurship-through-acquisition-europe

Join our 2026 CEO in Residence Cohort wadcap.com/join