What Makes a Successful CEO-in-Residence at WAD Capital?

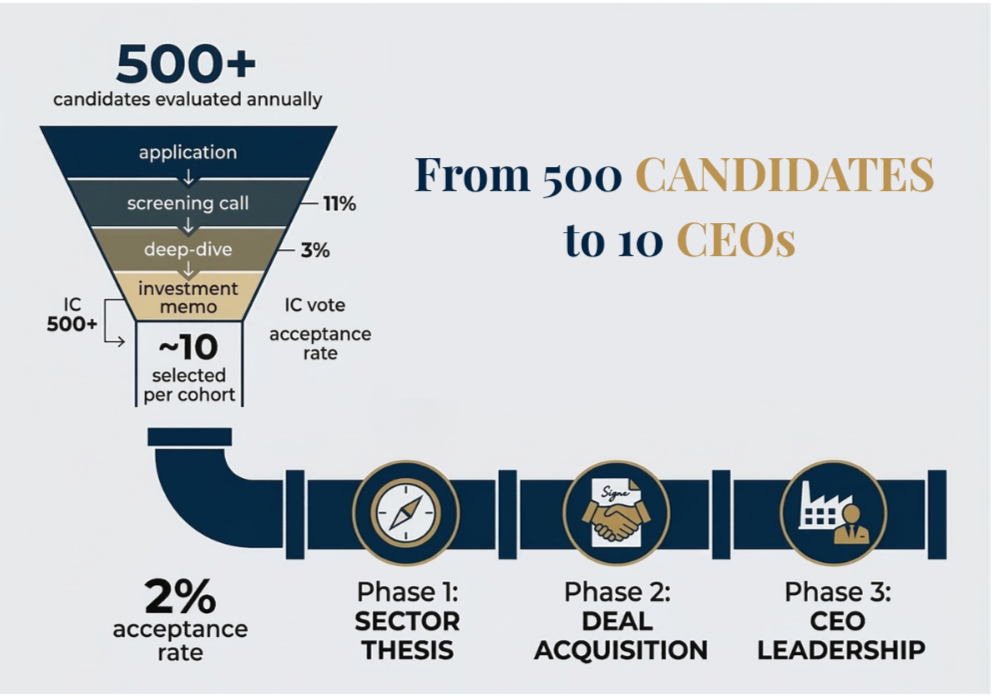

WAD Capital evaluates more than 500 executive candidates every year. Roughly ten make it through. The gap between those numbers tells you most of what you need to know about what separates a successful CEO-in-Residence from someone who looks good on paper but stalls when the work gets uncomfortable.

Entrepreneurship through acquisition has produced aggregate pre-tax returns of 35.1% IRR across 681 funds tracked by the 2024 Stanford GSB Search Fund Study. Those returns are real. They are also the output of a process that grinds through people who underestimate what "find, buy, and run a company" actually demands across twelve to twenty-four months of sustained, unglamorous effort. The CIR programme at WAD Capital is designed around that reality, and the people who thrive in it share a set of traits that become visible long before they sign their first acquisition.

Entrepreneurship Through Acquisition Demands a Specific Kind of Person

Most candidates who approach WAD Capital have impressive CVs. Tier-one consulting, operational leadership at recognisable firms, MBAs from schools that rank well. None of that is disqualifying. But none of it is sufficient either.

The selection pipeline runs from online application through a screening call, then a deep-dive session with a partner, followed by the production of a 10-to-15-page investment memo laying out a sector thesis and acquisition strategy. That memo gets presented to the partnership. Then the investment committee votes. Plenty of accomplished people drop out between the screening call and the memo, because the memo is where you stop talking about what you've done and start proving you can think independently about where capital should go.

A successful CIR at WAD has what we call a credible "right to win" in a specific vertical. That means deep industry experience, a specialised network, or domain knowledge that gives you an informational edge over generalist buyers when you're evaluating a €2M EBITDA metal fabrication business in Charleroi or a fire safety specialist in Walloon Brabant. Generalists who want to "explore opportunities" tend to produce memos that read like McKinsey decks. Practitioners who have spent fifteen years in HVAC or pharmaceutical distribution or logistics produce memos that reveal where the real margins hide and which owners are approachable.

The 2024 IESE International Search Fund Study tracked 320 search funds outside the U.S. and Canada and found international searchers achieving acquisition success rates outperforming the 63% domestic rate, with a record 59 new funds formed in 2023. The model works at a population level. But that tells you nothing about whether a specific individual will succeed in a specific market with a specific thesis.

Phase One: Building Your Sector Thesis

The first three months of the CIR programme look nothing like what most candidates expect. No deal flow. No LOIs. No spreadsheets full of targets. Instead, you are defining the sector where you will spend the next decade of your career, and defending that choice against partners and peers who are not inclined to be gentle about gaps in your logic.

Your sector thesis is the intellectual foundation for everything that follows. Pick too narrow and you will run out of targets within 300 kilometres of Brussels. Pick too broad and you will struggle to articulate why a specific seller should trust you with the business they spent thirty years building. The tension between those two failure modes is where good theses live.

WAD's Deal Intelligence platform accelerates the mechanical parts of this work. Financial profiles, automated screening, intelligent filtering across thousands of potential targets. What the technology cannot do is replace the judgment calls. Should you target a fragmented market where five add-on acquisitions might create a regional leader? Or a concentrated one where a single platform acquisition gives you immediate scale? Those questions require someone who has operated in the sector, not someone who can build a pretty slide about it.

Residents who move through this phase well tend to share a habit: they talk to owners early, before they have a target, just to understand how the market works at the level of individual businesses. They learn which Belgian banks lend to SME acquirers in their sector, what multiples are realistic for a business with €1.5M EBITDA in B2B services, and which brokers have deal flow worth seeing.

Phase Two: Finding and Closing Your Deal

Sourcing, evaluating, and acquiring a company within nine to twelve months is achievable but not automatic. KfW Research reported in 2024 that 30% of German SME owners are already at least 60 years old, and approximately 125,000 successions are needed per year through 2027 in Germany alone. Plenty of businesses need new leadership across Europe. Getting from "theoretically available" to "signed SPA" is where most of the difficulty lives.

You might screen 200 companies, have meaningful conversations with 40, conduct preliminary due diligence on 10, and submit an LOI on 3. One of those LOIs turns into a deal, maybe. Residents who close well kill bad deals quickly rather than nursing marginal opportunities because they have invested emotional energy in them.

The cohort structure matters here in a way that is hard to appreciate until you are inside it. In a traditional solo search fund, your sounding board is your investors and whatever advisory board you've assembled. At WAD, your weekly cohort call puts your deal in front of ten to fifteen peers who are going through the same process in adjacent sectors. When someone in packaging spots a revenue concentration risk in your target's customer base that you had rationalised away, that is uncomfortable. It is also the kind of feedback that prevents you from buying a business that craters in year two.

WAD provides 100% of acquisition financing. No personal capital required (though co-investment is encouraged). This removes the financial desperation that causes some self-funded searchers to close on marginal deals because they cannot afford to keep searching. According to the 2024 Stanford GSB Search Fund Study, the acquisition rate for core search funds has been consistently around 57% since 2014. Having the financial runway to be selective is a structural advantage, but it only works if the CIR exercises that selectivity rather than treating capital availability as permission to move fast on weak opportunities.

Phase Three: Walking In as CEO on Day One

Closing the acquisition is roughly the halfway point of the hard work. Maybe less.

The day you take over as CEO, every employee watched the founder leave and is now evaluating whether you deserve the chair. Your CFO (if there is one; in a €3M EBITDA business, the "CFO" is sometimes a bookkeeper and an accountant who visits monthly) has relationships with the bank that predate you by fifteen years. Your largest customer has the founder's personal mobile number. Your warehouse manager has been doing things a particular way since 1997.

Successful CIRs in this phase do not walk in with a 90-day transformation plan. They walk in with questions. They spend the first weeks understanding cash flow patterns, customer dependencies, operational bottlenecks, and the informal power structures that the org chart does not capture. Frédéric Schilling's acquisition of Groupe Jordan in Hainaut is instructive here. The founder, Jean-Luc Stavaux, reinvested in the business and stayed on as Sales & Marketing Director. That kind of continuity does not happen because you presented a compelling PowerPoint. It happens because the seller trusts that you understand what they built and will not wreck it.

More about Frédéric wadcap.com/residents/frederic-schilling

Post-acquisition, the CIR role shifts to a CEO role with competitive salary, bonus scheme, and equity stake. WAD Capital holds 80% and the CEO partner holds 20%, vested in three stages based on value creation. Buy-and-build strategies become possible case by case. Steven Bourgeois at Omnisecur Group is building a platform in fire safety where stricter regulations create structural growth for a consolidator. That kind of vision only matters if you first earned the operational credibility to execute it.

More about Steven wadcap.com/residents/steven-bourgeois

The full playbook for what those Day-One questions actually look like, and how to manage the people dynamics they surface, is covered here: https://wadcap.com/blog/first-90-days-ceo-leadership-transition-sme

What the Cohort Model Actually Changes

The DIHK (German Chambers of Industry and Commerce) has established that the number of business owners seeking succession solutions is three times higher than the number of interested buyers. European SMEs need leadership. The pipeline of qualified acquirer-operators is the bottleneck.

WAD's cohort model addresses this differently than a traditional search fund. Ten CEOs selected in parallel, sharing learnings across sectors, accessing the same Generative DealFlow™ technology for deal sourcing, and benchmarking their progress against peers at the same stage.

A resident working on an energy transition thesis can learn from a peer's experience negotiating a deal in healthcare about structuring seller reinvestment. Someone evaluating a logistics platform can borrow due diligence frameworks tested on a packaging acquisition. These are not theoretical synergies. The cohort compresses the learning curve that traditionally stretches solo searchers to 18-24 months into something closer to 6-12, because most of the infrastructure (legal and financial templates, CRM and pipeline software, marketing materials, weekly mentorship from partners) is waiting on day one rather than being built from scratch.

The 2024 Stanford study noted growing adoption of accelerator and entrepreneur-in-residence models alongside traditional core search funds. WAD's model sits in this institutional ETA category, with the added dimension of a cohort and proprietary technology that most EIR programmes lack.

Who This Programme Is Not For

Honesty about fit matters more than recruitment volume. The CIR programme is a full-time, twelve-month minimum commitment (extendable to twenty-four) requiring geographic flexibility within roughly 300 kilometres of Brussels. Target businesses are in the €1-5M EBITDA range across B2B services, energy transition, healthcare, and other fragmented markets. These are not startups. The work is making something good run better, not inventing something from nothing.

If your motivation is primarily financial, you will find the search phase tedious and the operational phase frustrating. The financial outcomes in ETA can be excellent (WAD targets an IRR of 34-35% based on historical search fund model returns) but they materialise over a five-to-ten-year horizon through accumulated operational improvements, not a quick flip.

If you cannot tolerate ambiguity, the search phase will be miserable. You will spend months evaluating businesses where the financials are presented in a format that would make any auditor cringe, where the seller's motivations shift between conversations, and where deals fall apart for reasons unrelated to your analysis. CIRs who navigate this well treat dead deals as data rather than failure.

And if you are not willing to deeply respect what a founder built over thirty years, even when you can see exactly where they underinvested and what you would do differently, this programme will not work for you. European SME succession is a human transaction first and a financial transaction second.

WAD Capital is building Cohort 2026. Applications are open for executives with 10+ years of relevant sector experience and a credible thesis in a fragmented European market. The selection process is rigorous and the work demanding. If that fits what you are looking for,apply through wadcap.com/join or review the programme details atwadcap.com/faq.