Why Entrepreneurship Through Acquisition Takes 20 Months? (and How to Cut That in Half)

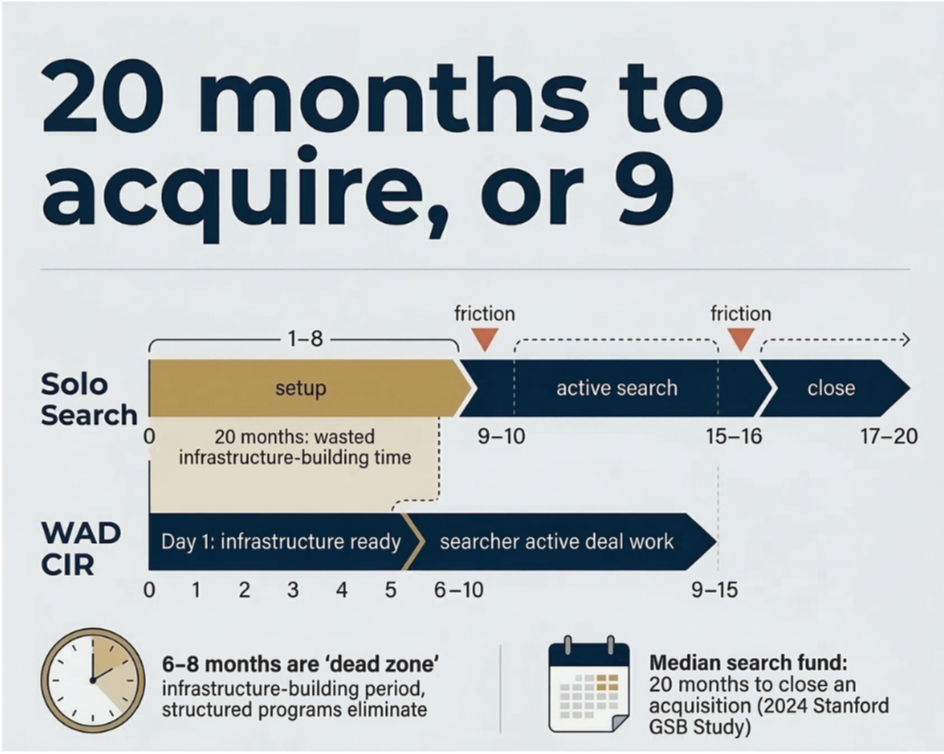

The median search fund takes 20 months to close an acquisition, according to the 2024 Stanford GSB Search Fund Study. Most of that time isn't spent evaluating companies. Aspiring acquisition entrepreneurs burn through their first six to eight months building the infrastructure to evaluate companies, financial models, legal templates, sourcing networks, a CRM that should have been configured before they ever wrote an outreach email. By the time a solo searcher has a functioning pipeline, a structured programme has already moved three candidates into exclusivity.

This distinction matters more than the ETA community typically acknowledges. A record 94 core search funds launched in 2023 alone, and competition for quality €1–5M EBITDA businesses is intensifying across Europe, particularly in the fragmented B2B services, energy, and healthcare sectors where the best targets sit. Speed to close is increasingly a competitive advantage, not a luxury.

What 20 Months of Searching Actually Looks Like

Consider the traditional search fund calendar. Month one through three: raise search capital, incorporate your vehicle, hire a lawyer, build your financial model from scratch. Month four through six: start outreach, realise your target list is too broad, refine your sector thesis, rebuild your target list. Month seven through twelve: run a proper pipeline, get into a few processes, lose two deals because your diligence was slower than the competition's. Month thirteen through twenty: finally close something, if you're in the 63% who manage to acquire at all.

That 63% figure comes from the same Stanford study. Roughly four in ten search fund entrepreneurs never acquire a company. Some run out of search capital. Others get outbid. Many simply lose momentum after eighteen months of grinding through a process they had to invent as they went.

The international picture is similarly instructive. The 2024 IESE International Search Fund Study now tracks 320 international search funds, with 85 acquisitions completed in Europe. European searchers face additional complexity, multilingual negotiations, fragmented legal regimes across jurisdictions, and a seller demographic that skews older and more cautious than their North American counterparts. According to KfW Research (2024), 30% of German SME owners are now over 60, and roughly 125,000 businesses need a successor every year in Germany alone. Across the EU, approximately 450,000 firms employing 2 million people change ownership annually, with an estimated 150,000 facing the risk of an unsuccessful transfer (European Commission, Network of SME Envoys, 2024).

These sellers aren't browsing deal platforms looking for a first-time searcher who incorporated last Tuesday. They want to know who's sitting across the table, who's financing the deal, and whether the transition plan is real.

The Infrastructure Problem Nobody Talks About

Every published guide to entrepreneurship through acquisition walks you through the search phase in satisfying detail. Raise capital. Build a thesis. Source deals. Negotiate. Close. What they consistently understate is how much invisible infrastructure separates a fast, successful search from an 18-month slog.

A solo searcher in month three is still debating which CRM to use. A solo searcher in month six is learning (the hard way) that their outreach templates read like a private equity cold call and that Belgian SME owners don't respond well to institutional language. By month nine, they've figured out how to run a proper vendor due diligence workstream, but they've already lost two promising targets to better-prepared buyers.

The pattern repeats across nearly every first-time searcher. Not because they lack talent or drive, the people pursuing this path are typically accomplished executives with a decade or more of operating experience. The bottleneck is tooling and process. Nobody hands you the playbook. You write it yourself, on the clock, while the search capital burns.

What a WAD CIR is doing in those same three weeks instead, the structured investment memo, the 500-company market mapping, the minimum-five expert interviews, is laid out here: https://wadcap.com/blog/sector-selection-sme-acquisition-investment-thesis

An SME Acquisition Program Built for Speed

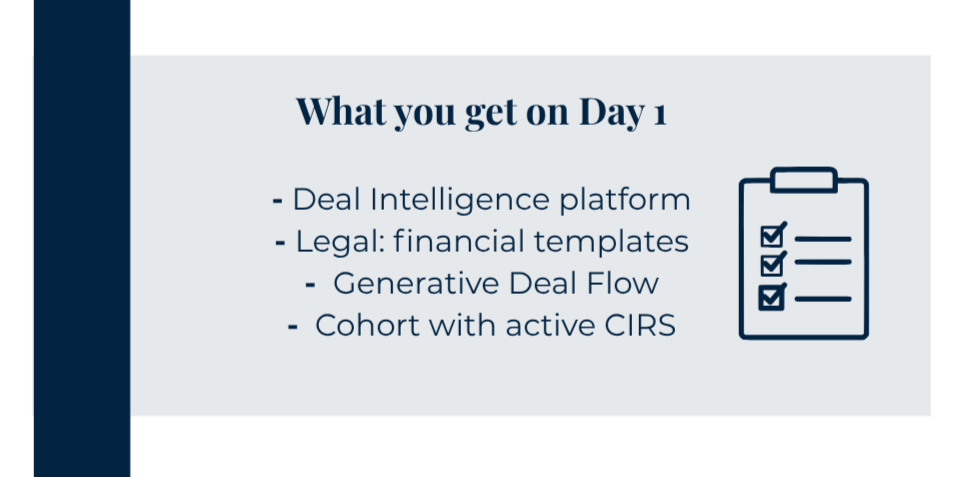

WAD Capital's CEO-in-Residence programme was designed around a specific observation: the most recoverable time in a search isn't the negotiation phase or the diligence phase. It's the setup phase. Everything a solo searcher spends months building from scratch, deal sourcing infrastructure, financial modelling templates, legal frameworks, outreach systems — already exists inside WAD's platform when a new CIR joins the cohort.

On your first Monday as a CEO-in-Residence, you get login credentials to a Deal Intelligence platform with 60,000 companies already screened and filtered. Legal and financial templates tested across multiple completed acquisitions are ready in your shared drive. Your CRM is pre-configured for deal flow tracking, not adapted from some generic sales pipeline. Generative DealFlow™, WAD's AI-powered sourcing mechanism, is already running, combining data analytics, automated screening, and network-driven identification to surface targets you'd take weeks to find manually.

That's before you factor in the cohort effect. Fifteen active CEOs-in-Residence working across different sectors, comparing notes on weekly Thursday calls. Someone three months ahead of you walks through how they handled a vendor diligence issue with a retiring owner who was nervous about confidentiality.

Someone who just closed shares the specific language that worked in their LOI. This kind of institutional learning compounds. A private equity CEO program that isolates you with a mentor and a phone line produces a fundamentally different velocity than a cohort where hard-won knowledge circulates in near real time.

The result is a search that compresses into 9 to 15 months, against the traditional search fund benchmark of 20 months reported by Stanford, and the 24+ months common in European contexts where cross-border complexity adds friction.

If you want to know more visit our FAQs page wadcap.com/faq

The Part After the Signature: Why Most ETA Programmes Stop Too Early

Closing the deal is maybe 40% of the challenge. Running the company you just acquired is the other 60%, and this is where most entrepreneurship through acquisition frameworks go quiet.

You've signed. You own a €2M EBITDA industrial services company in Walloon Brabant. The founder is staying on for six months as a consultant. Forty-seven employees are watching to see whether you're going to gut the place or respect what they've built. Your first board meeting is in three weeks. What's your 100-day plan?

WAD's operations team doesn't disappear after closing. A dedicated CFO function steps in to direct financial strategy, governance, and risk management, not in an advisory capacity, but operationally. Market intelligence analysts verify industry data points so your strategic decisions are grounded in current numbers, not the founder's 2019 recollections. Your Deal Intelligence access continues, now repurposed for add-on acquisition scouting if a buy-and-build thesis makes sense in your sector.

WAD's post-acquisition philosophy follows a specific sequence. Observation first, spend time understanding culture, operations, and customer relationships before changing anything. Strengthen processes and governance to secure profitability. Then (and only then) pursue digitisation as a growth enabler, transforming what was a strong legacy company into a digitally enabled business. The point is restraint. An SME acquisition program that celebrates speed to close but ignores the delicate months after is optimising for the wrong metric. The founder who reinvests and stays on as an advisor (as Groupe Jordan's Jean-Luc Stavaux did after WAD's first acquisition) needs to trust that this transition preserves what he spent thirty years building.

What the 2026 Cohort Gets on Day One

WAD Capital is recruiting 10 new CEOs-in-Residence for the 2026 cohort. The pitch is straightforward: full acquisition financing (no personal capital required), a 20% equity stake vesting in three stages tied to value creation, and a structured programme designed to compress what the Stanford data says takes 20 months into a focused 9-to-15-month search backed by institutional infrastructure.

But the sharper pitch is what happens after the deal closes. You don't become a solo operator managing a €3M EBITDA company with a phone and a spreadsheet. You get an operations team that handles financial governance, market intelligence, and technology, functions that would take a standalone CEO months to hire for and years to build internally. You get a cohort of peers running companies across transportation, healthcare, packaging, energy transition, fire safety, engineering services, and circularity, all navigating the same first-year challenges in parallel.

European SME succession is accelerating. The demographic data from KfW, the European Commission, and DIHK all point the same direction: the wave of retiring founders is growing, the pool of qualified successors is not, and the businesses caught in between represent millions of jobs and billions in economic output. The executives who position themselves inside a structured programme now will have their pick of quality targets. Those who spend 2026 building infrastructure from scratch will be competing for whatever's left in 2028.

Applications for the 2026 cohort are open at wadcap.com/join.