What Makes a Sector Right for Acquisition? How CIRs Build Their Investment Thesis

A sector suitable for SME acquisition through entrepreneurship through acquisition has four defining characteristics: fragmentation (no dominant consolidator, typically many operators below €5 million EBITDA within a defined region), structural demand drivers that are independent of economic cycles, recurring or contractual revenue at the company level, and an ageing owner base actively seeking succession. WAD Capital's four acquisitions across 2025 and early 2026 each satisfy all four. Kaeron targets Belgium's fragmented HVAC market, where energy transition regulation creates structural demand and no single operator holds dominant regional share. OmniSecur operates in Belgian physical security installation, shaped by tightening compliance mandates. NexVolta positions in electrical works tied to Belgium's electrification push.HBI Tyres and Wheels is a specialist niche manufacturer with proprietary brands in agricultural and industrial tyres. Fragmentation and structural tailwinds are the two non-negotiable criteria. The others follow from them.

What Are the Four Characteristics of an Acquisition-Ready Sector?

Fragmentation. The single most predictable indicator of a viable acquisition market. Fragmentation means dozens of owner-managed businesses serving the same end market with no single operator holding dominant regional share. It means a first acquisition gives you a platform, not a ceiling. It means add-on targets exist within 300 kilometres of Brussels. It also means the sector has not yet attracted serious private equity attention, which keeps entry multiples at levels where the economics of a €1 to €5 million EBITDA acquisition actually work.

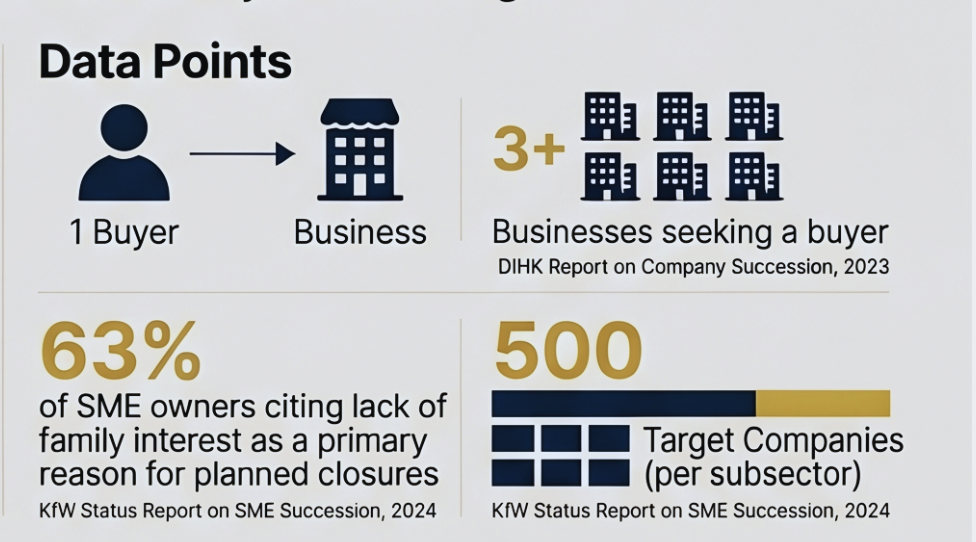

The DIHK, Germany's Chambers of Industry and Commerce, found that for every individual interested in acquiring a business, more than three businesses are already seeking a buyer, according to the DIHK Report on Company Succession, 2023. That ratio holds across most Western European markets. The problem is not a shortage of businesses. Fragmented sectors are where this imbalance is most acute, because they house the highest concentration of owner-managed companies with no institutional buyer infrastructure in place.

Structural demand drivers. A sector with a good business available is not the same as a sector where the business will be worth more in five years. Structural tailwinds are what separate the two. Regulation tightening, energy transition mandates, ageing population service demand, digitalisation requirements in analogue industries — these are the mechanisms that drive demand independently of whether the economy has a good quarter. A CIR who acquires into structural growth is not betting on their own sales ability alone. The sector is doing part of the work.

Recurring or contractual revenue. Maintenance contracts, service-level agreements, long-term public sector frameworks. At the company level, this is what makes a €1.5 million EBITDA business a predictable asset rather than a lumpy one. Dealsuite's European M&A Monitor for H2 2024, published March 2025, reports that the average European EBITDA multiple sits at 5.25x, but businesses generating €200,000 in EBITDA trade at approximately 3.9x while businesses at €10 million EBITDA trade at 7.2x. The multiple gap between small and large reflects perceived risk. Recurring revenue is the primary mechanism for compressing that risk at the company level.

An ageing owner base. A fragmented sector with structural demand and recurring revenue still requires willing sellers. Succession pressure is the fourth criterion, and in most B2B services markets across Belgium, the Netherlands, and northern France, it is not hard to find. The demographic trajectory is fixed. The question is whether a specific subsector has a sufficient density of owners at or approaching retirement age to sustain deal flow across a 12 to 24-month search.

Getting that sector call right is precisely what separates the searchers who close in 9 to 15 months from the 20-month median reported by Stanford's 2024 Search Fund Study — a thesis built on a genuinely fragmented, demand-backed sector doesn't just find better companies, it finds them faster."

None of the four criteria operate in isolation. A sector with fragmentation but no structural tailwind produces a cheap business in a declining market. One with structural demand but no fragmentation means you are competing against established operators who have already consolidated the obvious targets. The combination is what makes a thesis defensible rather than aspirational.

What Does a Strong Investment Thesis Actually Look Like?

It is a 10 to 15-page document, not a slide deck. It covers the sector's structure, identifies the acquisition target profile, explains why the specific CIR candidate has a credible right to win in that vertical, and outlines a concrete value creation plan across a five to seven-year hold period. WAD Capital's investment committee reads this document before a programme contract is signed.

That sequence matters. The thesis is not written after joining the programme. It is the filter for entering it.

A credible right to win is not a general interest in a sector. It is deep industry experience that gives you an informational advantage when evaluating a specific company. Frédéric Schilling, who leads Kaeron, spent 30 years in RACHP across industrial multinationals including P&G and Goodyear. He understood decarbonisation and energy transition before selecting HVAC as his sector. Steven Bourgeois, who leads OmniSecur, spent 17 years in management and consulting across B2B and industrial sectors, with a specialist focus in fire safety systems and security solutions. He had managed the P&L of a France-Benelux subsidiary. Neither man wrote a generic thesis about "opportunities in the Belgian services sector." Both identified a specific market structure and then explained, precisely, why they were better positioned than a generalist buyer to evaluate and run a company within it.

Guy-Louis de le Vingne, who leads NexVolta, built his thesis around the energy transition value chain before selecting Mignone SA in Manage, Hainaut, as the platform. Mignone had 35 years of construction and electrical installation work and 75% of revenue from public sector clients. A generalist buyer sees a 35-year-old construction company. Someone who has spent years analysing the full energy transition stack — solar, heat pumps, EVs, building renovation, AI infrastructure requirements — sees a business that has spent three decades building exactly the technical credentials that electrification mandates will make scarce.

The thesis came first. The target fit the thesis. That ordering is not accidental. It is the point.

How WAD Capital CIRs Build Their Sector Thesis in Practice

The first three weeks of the programme are spent on Step 1: Investment Memo Creation. The objective is to develop a detailed memo covering search scope, target value propositions, growth projections, and financial health. Week one is deep-dive market research — industry data, analyst reports, competitive metrics. Week two is the draft, focusing on structural growth drivers and upcoming regulation. By week three, the CIR has conducted a minimum of five industry expert interviews to validate the thesis.

That last requirement is worth pausing on. Five structured conversations with people who operate in the sector — not LinkedIn messages, not desktop research. Conversations that reveal which Belgian banks lend to acquirers in this space, what multiples are realistic for a business with €1.5 million EBITDA, which owners are approaching retirement and have no succession plan, and where the margins actually hide versus where the pitch decks claim they are. The KPI for Step 1 is investment memo delivered and approved by WAD Capital's investment partners. Not submitted. Approved.

Step 2 is Market Mapping and List Creation, running from weeks four to six. The objective is to identify 500 potential target companies per subsector within 300 kilometres of Brussels. Week four is research aligned with the investment scope. Week five is prioritisation by investment size, strategic alignment, and likelihood to sell. Week six produces the finalised target list and a market map of key players. The KPI is 250 companies identified within the fund's investment scope per subsector — the 500-company target covers the full mapping exercise across primary and adjacent sub-markets.

This is not how generalists approach acquisition. Someone who decides they want to "buy a business in Belgium" and starts browsing broker listings has no idea what they are looking for until they see it. A CIR who has mapped 500 companies across a subsector, spoken to five industry experts, had the thesis stress-tested by WAD's partners, and produced an approved investment memo has a fundamentally different relationship with the market. They know which categories of companies to prioritise. They can assess a target in hours rather than weeks. They know which red flags to look for in the first conversation with an owner, and which of those red flags are structural problems versus negotiating levers.

WAD Capital's Generative DealFlow™ platform accelerates the mechanical parts of this work. Financial profiles, automated screening across thousands of potential targets, intelligent filtering by sector, size, and geography. The technology does not replace the judgment calls. It compresses the time between identifying the universe and reaching the conversations that matter.

What Separates a Defensible Thesis from a Wishlist?

Most weak theses fail on one of three specificity dimensions.

The first is geographic scope that exceeds the fund's parameters. WAD Capital operates within approximately 300 kilometres of Brussels. A thesis built on "European electrical services consolidation" is not a thesis. It is a research interest. The target density within 300 kilometres of Brussels, the seller profile in that market, the regulatory environment in Belgium and the Netherlands — these are the operational realities the thesis must address. Broad enough to sustain 18 months of deal flow. Specific enough that you can explain to a business owner in Walloon Brabant why you are the right person to take over what they built.

The second failure mode is a tailwind argument without a fragmentation foundation. Belgium is electrifying. Energy transition is real. But "I want to acquire in energy transition" describes half the companies in the CIR cohort's pipeline. The thesis needs to identify the specific subsector within that transition where fragmentation is highest, owner demographics are most favourable, and the CIR's background creates a genuine informational edge.

The third is a value creation plan that reads like a consulting deliverable. "Implement best practices, drive operational efficiency, pursue add-on acquisitions." Committees have read that document. What a good thesis includes instead is specific: which operational levers the CIR has pulled in prior roles, what the realistic integration timeline looks like for a first add-on in this subsector, which types of synergies are achievable between two businesses at this scale and which are not.

The investment committee at WAD Capital is not evaluating the sector. They know the sectors. They are evaluating whether the specific candidate has the domain knowledge and operational clarity to execute in it. Two people can write theses on Belgian HVAC consolidation. The one who spent 30 years in the industry and can name which certifications matter for public sector contracts, which local procurement patterns create recurring revenue, and which types of owners are most likely to reinvest post-acquisition is the one who gets through the committee.

How Do You Know When Your Thesis Is Ready?

Three tests. Not checklists. Tests.

You can describe the ideal acquisition target — the sector, the revenue range, the revenue mix, the geographic footprint, the owner profile — in one paragraph without hedging. Not "we are open to various types of businesses" but "a B2B fire safety installer in Wallonia or Flemish Brabant, €800,000 to €2 million EBITDA, with at least 40% of revenue from maintenance contracts, owned by a founder over 60 with no obvious family succession plan."

You can explain, in the same conversation, why this sector in this geography at this size is underserved by existing buyers. Private equity is too large. Solo acquirers lack the capital and sector expertise. Family buyers are statistically declining in numbers, with 63% of SME owners citing lack of family interest as the primary reason for planned closures, according to the KfW Status Report on SME Succession, 2024. The thesis has to close that gap specifically.

You can tell a founder who asks why you should take over the business they spent 30 years building. The answer cannot be generic. It requires sector knowledge that earns credibility in the first meeting, an understanding of how the business actually works at the operational level, and a value creation plan that treats what the founder built as the foundation rather than a problem to be fixed.

If the thesis passes all three tests, it is probably ready for the investment committee. If it passes two, it needs another week of industry conversations. If it passes one, it is a research interest, not an investment thesis.

WAD Capital evaluates more than 500 executive candidates annually to build a cohort of approximately ten CEOs-in-Residence. The selection ratio exists because the thesis is the filter. An impressive CV narrows you to the screening call. The investment memo is where the committee learns whether you are the operator who will close a good deal or the executive who will spend 18 months searching and walk away with nothing.

What the committee weighs beyond the memo itself, and what separates a candidate who closes a good deal from one who walks away empty-handed, is covered here: https://wadcap.com/blog/what-makes-a-successful-ceo-in-residence-at-wad-capital

Applications for the 2026 cohort are open. Programme details and the application process are atwadcap.com/join-cir andwadcap.com/faq