Why Family Businesses in Europe Cannot Find Internal Successors

The majority of European SME owners prefer to hand their business to a family member. Most of them cannot. According to the 2024 KfW Nachfolge-Monitoring Mittelstand study, 63% of owners who ultimately close their business, rather than transfer it, cite lack of family interest as the primary reason. That figure rose by 13 percentage points in a single year. The businesses closing are not failing companies. They are profitable, often decades old, with established client relationships and experienced staff. The European Commission estimates that 690,000 SMEs face ownership transitions each year across the EU, employing millions of people. The succession gap is not caused by business quality. It is caused by a generational shift in career preferences that has been building for thirty years and is now producing a large, concentrated wave of ownership transitions with insufficient candidates on the other side. WAD Capital's CEO-in-Residence programme exists specifically to match qualified, sector-experienced operators with succession-ready businesses across Europe.

Why Did Family Business Succession Work in Previous Generations?

For most of the twentieth century, inheriting a family business was a default career path for the children of business owners across Europe. It carried social status. It offered financial security. It required no academic credentials beyond the ability to learn the operations from the person who built them. The businesses were often tied to the physical and social fabric of specific towns: the HVAC company in Hainaut that had been warming the same public buildings since 1975, the electrical contractor in the Netherlands whose founder's son could name every municipal procurement officer in the province, the logistics firm in northern France that had run the same regional routes for forty years.

That world has not disappeared. It has changed. The generation of founders who built the current SME base across Germany, Belgium, France, and the Netherlands did so during an era when business ownership was a meaningful competitive option for educated, ambitious people. Today, the same children of SME founders are selecting careers in consulting, corporate management, technology, and professional services. Those careers offer better starting salaries, clearer progression paths, international mobility, and none of the operational responsibility that comes with running a 30-person service business in a regional market.

This is not ingratitude or lack of respect for what was built. It is a rational response to a changed labour market. The founders understand this, even when it is painful. Their understanding does not create a successor.

What Does the Successor Gap Actually Look Like Across Europe?

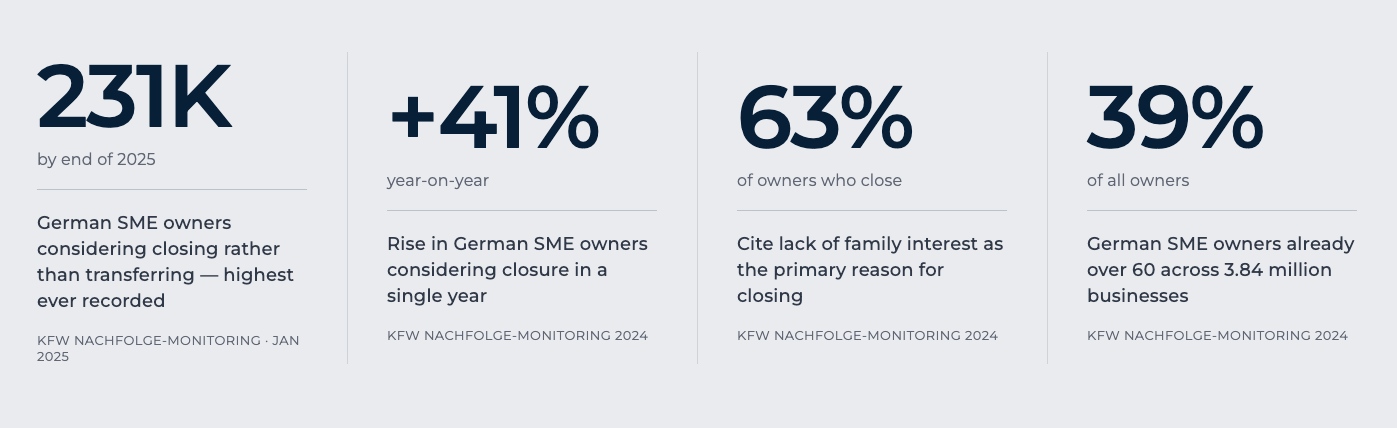

The data is most granular in Germany, where KfW Research has been tracking SME succession since 2015. Their January 2025 report found that 231,000 German SME owners were considering closing their businesses by the end of 2025, a 41% increase over the prior year and the highest figure ever recorded (KfW Nachfolge-Monitoring Mittelstand, 2024). Across Germany's 3.84 million SMEs, 39% of owners are already over 60. The average owner age is 54.

The same demographic trajectory runs through France, where an estimated 700,000 company transitions are expected in the next decade. Across the continent, the DIHK (German Chambers of Industry and Commerce) calculates that for every individual who contacts a chamber of commerce interested in acquiring a business, more than three businesses are already there looking for a buyer. That ratio has been widening consistently since 2012 (DIHK Report on Company Succession, 2023).

The Dealsuite European M&A Monitor (H2-2024) captures what happens when these businesses actually reach the market. Across Europe, 32% of sell-side assignments are discontinued before completion. The most common cause is a gap between what founders expect and what the market will pay. The second most common cause is that no qualified buyer materialises at all.

What Does the Succession Gap Look Like Specifically in Belgium and the Netherlands?

The Benelux sits inside the European pattern but with distinct local dynamics worth understanding separately.

Belgium's SME base employs 66.3% of the country's workforce, a higher share than France, the Netherlands, or the EU average, according to the European Commission's SME Performance Review. That concentration means ownership transitions carry disproportionate local employment consequences. When a profitable Belgian SME closes rather than transfers, the impact lands directly in a specific town or region, not spread across a diversified economy. The share of Belgian SME owners over 60 grew from 12% in 2002 to 27% in 2018, according to European Commission and Eurostat base data. The trajectory has continued since.

The Netherlands shows different market mechanics but the same underlying pressure. The Dealsuite European M&A Monitor (H2-2024) records a Dutch business transfer close rate of 78%, among the highest in Europe and well above the DACH region at 62% or Central and Eastern Europe at 59%. The Dutch market's relative efficiency reflects stronger M&A advisory infrastructure and a larger pool of active acquirers per unit of deal flow. Even so, roughly one in five Dutch SME transfer processes does not complete. In a market with approximately 450,000 enterprises, that is a significant volume of businesses that start a transfer process and do not finish one.

The businesses that fail to transfer across both countries concentrate in the €1 to €5 million EBITDA range. Too small for institutional private equity. Too complex for a buyer without sector experience. Too valuable for the owner to simply close.

Why Does the External Successor Pipeline Not Naturally Fill the Gap?

The logical answer to "my children do not want the business" is "find someone else." Finding someone else requires solving three separate problems simultaneously.

The first is operational credibility. A retiring founder of a specialist industrial services company is not simply looking for someone willing to sign the purchase agreement. They are looking for someone who can walk into a meeting with a long-standing client, discuss the technical specifics of what the business delivers, and give that client reason to stay. Generic management competence is not the same as sector credibility. The client relationship that represents 15% of revenue has been built on 20 years of reliable delivery by people the client knows by name.

The second is capital access. Acquiring a €1 to €5 million EBITDA business requires acquisition financing. Most talented executives who might be excellent operators have not accumulated the personal capital to fund an acquisition, and individual bank loans for business acquisitions are complex to structure without institutional backing.

The third is process. Running a search for the right business to acquire while maintaining a senior corporate career, conducting due diligence across multiple targets, and managing the emotional complexity of a founder relationship is a multi-year undertaking. Most people who would be excellent successors to European SMEs have no mechanism to run that process efficiently.

These are structural barriers that the market has not historically provided tools to overcome.

What Does a Structured External Transfer Look Like for a Business Owner?

The succession handled through NexVolta and the acquisition of Mignone SA in Manage, Hainaut, illustrates how the external transfer model works when the process is designed carefully. Donato Mignone and Ida Gargano founded their construction and electrical installation business in 1987. Thirty-five years later, with public and private sector clients built over decades and a strong base of long-standing public sector relationships, the succession question was genuine: who has the sector expertise, the operational competence, and the commitment to preserve what was built?

Guy-Louis de le Vingne, the incoming CEO, had spent more than a decade in business transformation and operational excellence, with specific focus on the energy transition value chain. He did not arrive because he happened to meet the Mignones at the right moment. He arrived because WAD Capital's structured Market Mapping process had identified Mignone SA as a business that matched the thesis he had spent months developing: positioning an electrical works platform to serve Belgium's electrification push. The match was operational before it was financial.

For a retiring founder, that distinction matters. The person taking over was not a generic buyer optimising for price. He was an operator with a specific reason to be there, an understanding of why the business mattered, and institutional backing that allowed the transaction to close at a pace the founders controlled.

The same logic governs Kaeron, the HVAC platform built through the acquisition of Groupe Jordan in Hainaut. Frédéric Schilling's background in decarbonisation and energy transition made him a credible conversation partner for Groupe Jordan's regional clients from his first week on site. Jean-Luc Stavaux, the Groupe Jordan founder, reinvested in the new structure and remained involved after the transaction closed. Client relationships, regional market knowledge, and institutional credibility all stayed inside the company.

What Should a Belgian or Dutch SME Owner Do if There Is no Family Successor

Start the conversation before the urgency sets in. The founders who navigate external succession best are those who allow enough time for the process to proceed at a considered pace rather than under pressure from a retirement date, a health event, or a business running on the founder's energy alone.

An external operator-led succession is not a fast transaction. The CEO-in-Residence who will eventually acquire a business spends 12 months or more in structured search before identifying and approaching targets. That time is used for sector immersion, thesis development, and building the knowledge that makes a first meeting credible rather than awkward. The founder who understands this consistently describes the experience differently from one approached cold by a broker representing a financial buyer with no sector background.

WAD Capital operates as a Benelux private equity platform, focused within 300 kilometres of Brussels, covering Belgium, the Netherlands, and bordering areas of northern France and western Germany. The relationship-based nature of SME succession in these markets requires geographic proximity and genuine sector presence. The European succession problem is continental in scale. The transactions that actually close are local.

If you are a business owner starting to think about what comes next, the /care-profit page explains what WAD Capital's values commitment to acquired businesses means in practice. The /portfolio page shows the businesses that have already made this transition.