The Difference Between a Business That Sells and One That Closes

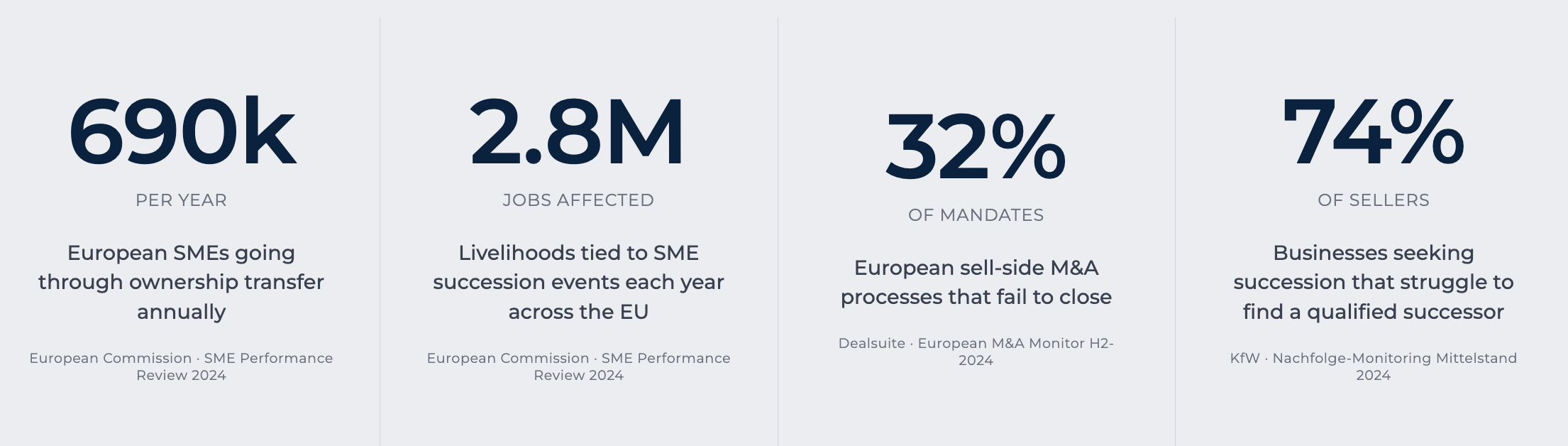

The difference between an SME that sells and one that closes when the founder retires is almost never the quality of the product or the loyalty of the customers. It is whether the business can function without the person who built it. Buyers evaluate transferability along four dimensions: how dependent the business is on the founder's personal relationships, how concentrated revenue is across customers, how documented the operational processes are, and whether a capable management layer exists beneath the owner. A business that holds up well across all four can be acquired, financed, and handed to a new operator. One that scores poorly on any of them faces a structural problem that price alone cannot fix. According to the Dealsuite European M&A Monitor (H2-2024), 32% of European sell-side mandates fail to close, and unrealistic valuation expectations are the leading stated cause but founder dependency is the underlying condition that makes those expectations unrealistic in the first place.

What Does "Transferable" Actually Mean for an SME?

Transferability is not about whether someone wants to buy your business. It is about whether a buyer can run it after you leave.

These are different questions. A buyer evaluating your company is not only assessing what it earns. They are assessing how much of what it earns depends on your continued presence. A business where the founder holds the key client relationships, approves every significant decision, and carries the pricing logic in their head is worth less to a buyer than an identical business on paper where those functions are distributed across a team. Not because the first business is poorly run. Because it cannot be transferred without losing a significant part of what makes it valuable.

The European Commission estimates that approximately 690,000 SMEs and 2.8 million jobs are affected by ownership transfers across the EU each year (SME Performance Review, 2024). A meaningful share of those transfers fail not because buyers are absent or financing is unavailable, but because the business as it exists cannot be separated from the person who built it.

Transferability is something a founder builds, mostly without realising it. The decisions that make a business harder to transfer are often the same decisions that made it successful:taking the important client meetings personally, pricing based on judgement accumulated over 20 years, keeping the best supplier relationships warm through a long-standing friendship. None of those are mistakes. They become problems only when the clock starts running on the handover.

How Does Founder Dependency Affect Whether a Business Can Be Sold?

A buyer who intends to operate your business needs to understand which parts of it work because of the systems and processes you built, and which parts work because of you specifically.

Client relationships are where this surfaces first. A client who has worked with you for fifteen years and renews annually without a formal contract is a relationship asset. Whether that asset transfers depends on whether the client's loyalty is to the business or to you personally. Often founders do not know the answer until a buyer asks. The honest diagnostic is blunt: if your five most important clients were told tomorrow that you were leaving and someone else was taking over, how many of them would take a call from a competitor that week?

That question is not hypothetical in a diligence process. Buyers model it. They will ask about client tenure, about whether relationships are documented, about whether the incoming operator has been introduced to key accounts before closing. A business where the founder has spent two years gradually transferring client relationships to a management team looks very different from one where the handover is supposed to happen on day one.

The same logic applies to pricing. If your margin depends on your personal judgement about what a client will accept, rather than a documented pricing framework, that margin is at risk the moment you step back. Buyers will discount for it. Buyers who are disciplined about how they value businesses will discount for it substantially.

What Role Does Customer Concentration Play in a Buyer's Decision?

Revenue concentration is the factor founders most consistently underestimate going into a sale process.

If your three largest clients account for more than half your revenue, a buyer sees a risk that is both quantifiable and difficult to mitigate quickly. Losing any one of those clients post-acquisition does not produce a proportional dip in performance. It produces a structural problem. Buyers will price that risk into their offer, and in some cases they will walk away entirely rather than accept the exposure.

The threshold that tends to trigger concern is a single client above 25 to 30% of revenue. Below that level, buyers can work with concentration through contractual protections and transition planning. Above it, the conversation about risk becomes the dominant conversation, and it tends to crowd out everything else.

Concentration in suppliers carries similar weight, though it attracts less attention. A business whose margin depends on a favourable agreement with one key supplier that was arranged through a personal relationship is exposed in the same structural way as one with a dominant client. The incoming operator inherits the relationship but not the history that produced the terms.

Geography matters too, in a specific way. A business operating across multiple client sectors and regions is more resilient to disruption during a transition than one serving a single industry in a single postcode. Neither is disqualifying. Both affect how a buyer models what happens in year one under new ownership.

Why Undocumented Processes Kill Otherwise Good Businesses at the Point of Sale

Most SME owners have never needed to write down how they do things, because they have always been there to explain it.

That works fine for thirty years of running the business. It becomes a critical problem the moment someone else needs to run it. A buyer who cannot see how decisions get made, how quality is maintained, how complaints are handled, and how new clients are onboarded is buying something they cannot fully evaluate. They are being asked to price a business partly on trust. Most buyers are not willing to do that at a fair multiple.

Documentation does not need to be a formal operations manual. It needs to be enough that a capable person stepping into the business on day one could understand how it functions without calling the previous owner every afternoon. Pricing frameworks, service delivery checklists, supplier contact lists with context, employee role definitions that reflect what people actually do rather than what their job titles say: these are the materials that make a business legible to a buyer.

The absence of documentation is also a signal buyers read as founder dependency in disguise. If nothing is written down, it is usually because the founder has always been the reference point for everything. That observation and the observation about founder dependency earlier in this post are, in most cases, describing the same underlying condition from two different angles.

What Does Management Depth Have to Do With Transferability?

A business with one layer of management below the founder is more transferable than one where the founder is effectively the entire management team.

This is not about headcount. A 20-person business can have genuine management depth if the right people have real authority and exercise it daily. A 60-person business can be entirely founder-dependent if every decision of consequence routes back to one person. Buyers are looking for evidence that the business can make decisions, resolve problems, and serve clients at its normal standard without the founder in the building.

The clearest version of this test is simple: what happened the last time you took two weeks off? If the answer is that you stayed reachable by phone and dealt with things remotely, that is useful information about what the transition will look like. If the answer is that nothing significant required your attention, the business has more depth than the average SME in your EBITDA range.

KfW's 2024 Nachfolge-Monitoring Mittelstand study found that 74% of businesses seeking succession cite finding a qualified successor as their primary challenge. The framing is usually about finding the right buyer. The operational reality, in many cases, is that the business itself needs to be made ready to receive one.

What Can a Founder Actually Do to Make Their Business More Transferable?

The honest answer is: quite a lot, but not in three months.

The changes that move the needle on transferability are structural, and they take time to produce evidence a buyer can see. A customer relationship that has been informal for a decade cannot be contractualised in the six weeks before a sale process opens. A management layer that does not currently exist cannot be built and proven capable in a quarter. A pricing framework written down for the first time the week before diligence reads exactly as rushed as it is.

Founders who achieve the best outcomes in a sale process — not just the highest price, but the cleanest process and the best fit with the incoming operator — are typically those who started making the business more transferable two to three years before they needed it to be.

The specific actions that matter most, in order of impact: reduce customer concentration by adding accounts; convert informal client relationships into documented agreements where possible; build a management layer that has real authority and exercises it visibly; document pricing logic, service delivery standards, and key supplier terms; and introduce a future operator to key clients before the transaction closes rather than after.

None of these are expensive. Most of them make the business better to run regardless of whether a sale ever happens. A business that does not depend on the founder to function at its normal standard is a better business, full stop. The transferability benefit is a consequence of that, not the cause.

What Does a Buyer Who Intends to Stay Look for Beyond the Balance Sheet?

Not every buyer approaches an SME acquisition the same way.

A buyer whose model is to acquire, extract value quickly, and resell in three years reads your business as a set of financial metrics. A buyer whose model is to acquire, install a qualified operator, and let the business compound over a decade reads it differently. They want to understand what the business does that no spreadsheet captures: the employee who has been there eighteen years and carries institutional knowledge about your largest client's decision-making process; the supplier relationship that produces better terms than any competitor can replicate because it was built through twenty years of reliability; the local reputation that means clients renew without shopping around.

These are the things that make a healthy SME worth more than its EBITDA multiple implies, and they are also the things most vulnerable to a badly managed transition. Mignone SA, founded in 1987 by Donato Mignone and Ida Gargano, had built 35 years of operating history and a stable public-sector client base before completing its succession through WAD Capital. The value in that business was not only in the financial statements. It was in the workforce, the long-standing client relationships, and the operational knowledge accumulated across three decades of construction and electrical work in Belgium. A buyer whose model involved replacing the management and cutting costs would have approached that asset very differently from one whose model is to find the right incoming operator and let the business continue growing under capable leadership.

WAD Capital's CARE-PROFIT framework, applied across all portfolio companies post-acquisition, is designed for exactly this context: businesses where value is embedded in people, culture, and relationships, not only in reported earnings. The framework is documented in full at/care-profit. For founders evaluating what responsible succession looks like in practice, the/portfolio page shows what completed transitions have produced.