How to Choose Between Starting a Business and Acquiring One

Should You Start a Business or Acquire One Instead?

Deciding between starting a business from zero and acquiring one through entrepreneurship through acquisition (ETA*) comes down to three questions, not one grand temperament test. How much unproven risk can you actually carry, financially and psychologically, for however long it takes to find out if anyone wants what you're building? How long can you go without meaningful income? And which of the skills you built over a corporate career actually transfer to the thing you're about to do? Founders answer these questions by trial. Executives considering ETA* through a programme like WAD Capital's CEO-in-Residence Programme can answer them before committing, which is the entire point of asking them first.

What Makes Starting a Business Different from Acquiring One?

A startup begins with a hypothesis. You believe a customer problem exists, you believe your solution solves it better than the alternatives, and you believe enough people will pay for it to build a business. None of that is known on day one. It's tested, iteratively, often for years, often with your own money.

An acquisition begins with a fact. The business already has customers who pay, an operating history you can read in three years of management accounts, and staff who show up and know how to run it. The uncertainty doesn't disappear. It moves. Instead of asking "does anyone want this," you're asking "can I run this better than it's currently being run, and can I do it without breaking what already works." That's a meaningfully easier question for someone who spent fifteen years managing P&L inside someone else's company, and a meaningfully harder one for someone who wants to build something that didn't exist before them.

How Much Risk Are You Actually Willing to Carry?

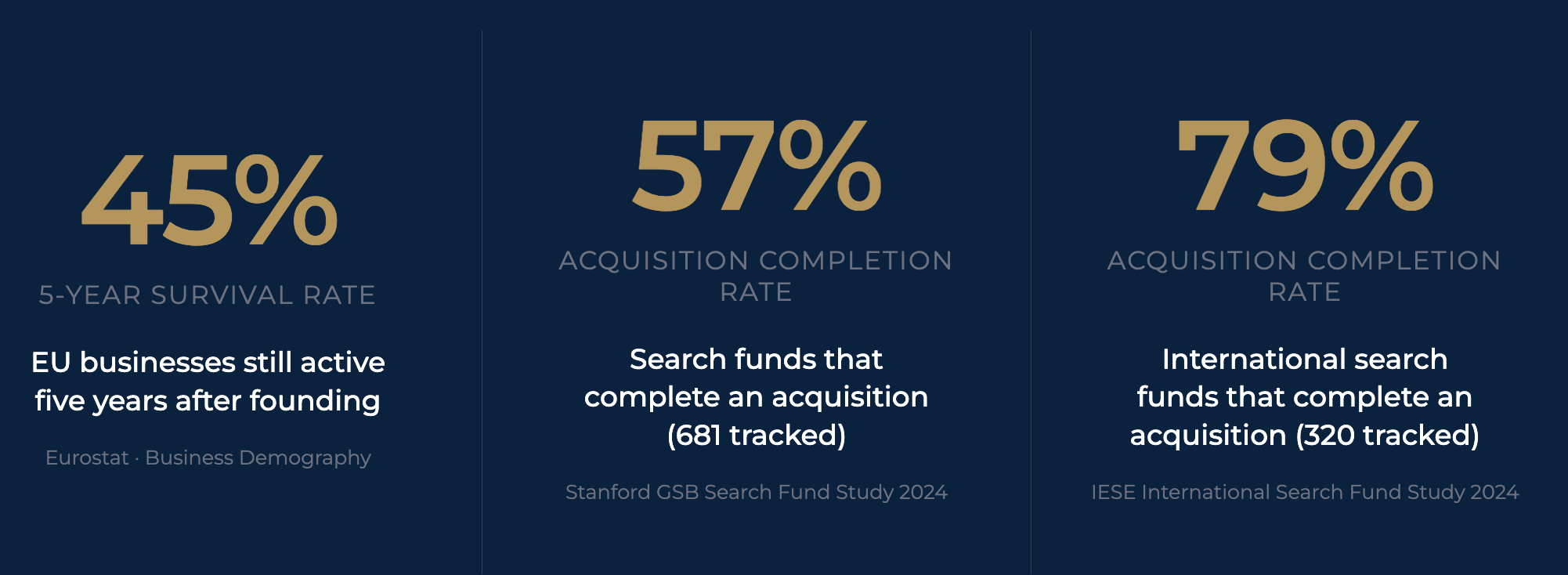

The honest answer is usually less than people think when they're still employed and imagining the leap. Eurostat's business demography data puts a number on what "unproven" actually costs: across the EU-27, only 45% of enterprises born in 2013 were still active five years later. Fewer than half. That figure includes plenty of businesses that failed for reasons that had nothing to do with the founder's competence, and plenty that failed for reasons that had everything to do with it. Either way, the founder absorbs that risk directly, usually with personal savings, often for two or three years before knowing whether the bet paid off.

ETA* doesn't eliminate risk. A business can still be poorly run after acquisition, a market can still shift, a key customer can still leave. What it removes is the specific risk of unproven demand, because the demand is already there before you sign anything. That's a different risk profile, not a lower-effort one. If what draws you to starting a company is genuinely the unproven idea, ETA* will feel like a compromise rather than a solution. If what draws you to entrepreneurship is running something and being accountable for its results, the unproven part was never the appeal to begin with.

Does Your Corporate Experience Actually Transfer to Founding, or to Operating?

This is the question most executives skip, and it's the one that predicts outcomes best. Building a startup rewards a specific and narrow skill set: rapid experimentation, comfort with ambiguity about whether the fundamental premise is even correct, and the ability to operate without most of the infrastructure a corporate career trains you to rely on. Fifteen years of P&L accountability, team leadership, and operational discipline doesn't disappear when you leave a corporate role, but it doesn't automatically transfer to product-market fit discovery either. Those are different muscles.

Acquiring and running an existing SME rewards almost exactly the skill set a senior operator already has. Reading financial statements, managing a team you didn't hire, improving processes that are already functional but not optimal, and negotiating with stakeholders who have existing relationships and expectations. Michaël Vandelaer moved from an executive role into acquiring and running HBI Tyres & Wheels, a Dutch manufacturer, through WAD Capital's programme, and became its CEO within nine months of starting the search. That timeline is achievable specifically because the operational skills required to run HBI were already skills he had. He wasn't learning how to run a business for the first time. He was applying an existing skill set to a new business.

What Does the Success Data Actually Show?

The 2024 Stanford GSB Search Fund Study recorded a 57% acquisition completion rate across 681 tracked funds, meaning a majority of people who commit to a search do eventually close a deal, though a meaningful minority don't. The 2024 IESE International Search Fund Study, covering 320 international funds including European activity, recorded a higher 79% acquisition success rate, a gap that likely reflects both a smaller, more recent dataset and the increasing role institutional support plays in European search outcomes.

Neither figure is directly comparable to startup survival data, because a search that doesn't end in an acquisition isn't the same kind of failure as a business that closes after two years of trading. But the shape of the comparison holds. Acquisition entrepreneurship carries execution risk concentrated at the search and close stage. Startup entrepreneurship carries existential risk that persists for years after you've already committed capital and time.

Is Entrepreneurship Through Acquisition Right for You?

If you want to build something that didn't exist before you, and you can tolerate multiple years of unproven demand while you find out whether it will, starting a business is the honest answer. If what you actually want is to run a business, be accountable for its performance, and own a meaningful stake in the outcome, without betting years of your career on whether the product concept itself works, entrepreneurship through acquisition is worth understanding properly before you rule it out or assume it's the easier path. It isn't easier. It's a different set of problems, better matched to a different set of skills.

The full mechanics of how WAD Capital's CEO-in-Residence Programme works, including financing, timeline, and selection, are documented at /faqs/ceo-in-residence. Applications for Cohort 2026 are open at /join-cir.