Selling Your Business in Belgium: What Retiring Founders Actually Need to Know

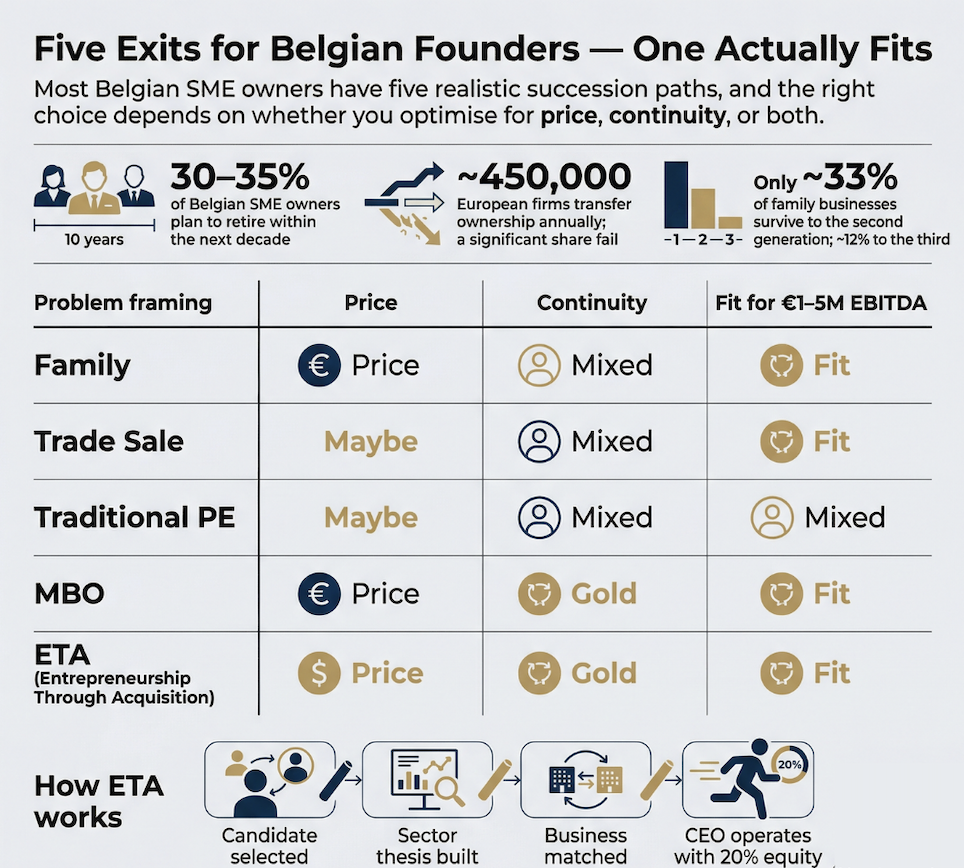

Somewhere between 30 and 35 percent of Belgian SME owners plan to retire within the next decade, according to European Commission SME data. Most of them have not yet decided who or what comes next.

The window matters. Across Europe, approximately 450,000 firms employing around 2 million people transfer ownership each year, and a significant share of those transfers fail, according to the European Commission's assessment of business transfer frameworks. Not because the businesses are unviable. Because the process was underprepared.

This guide is for Belgian founders in the €1 to €5 million EBITDA range who are starting to think seriously about their options. It covers the five realistic paths, what each one actually means in practice, and where WAD Capital fits in that landscape.

The succession problem no one talks about plainly

Belgian SMEs in the €1 to €5 million EBITDA band occupy an awkward position in the market. Too large to attract most individual buyers with personal capital. Too small to interest the large buyout funds, which need deployment at scale. The M&A advisory infrastructure that serves the upper mid-market does not translate well to businesses of this size, and the local accountant who has been doing your year-end for fifteen years is not necessarily equipped to run a sale process.

The result is that many perfectly sound businesses either sell below their worth, transfer to a family member who was not quite ready, or close outright when the founder retires. According to the European Commission, roughly a third of family businesses successfully transfer to the next generation, and only around 12 percent survive to a third generation. These are not bad businesses. They are businesses without a clear mechanism for the handover.

Option 1: Family succession

For many founders, this is the default assumption. One of the children takes over, the business stays in the family, the founder steps back gradually. When it works, it works well. The incoming leader already knows the culture, the key customers, the team dynamics. The transition can be managed over years rather than months.

The honest complications are worth naming. Capability and desire are separate questions. A child who has the operational ability to run the business may not want to, and a child who wants to run it may need significant development before they are ready. Forcing the issue creates resentment on both sides and often damages the business in the process. Family dynamics that existed before the succession tend to intensify during it, not resolve.

Family succession also does not typically solve the founder's liquidity position. You may transfer ownership while remaining financially exposed, particularly if the business carries debt or if the transaction is structured as a deferred payment over time. If capital diversification matters to you at this stage of life, family succession alone does not address it.

None of this means family succession is wrong. It means it needs to be stress-tested honestly rather than assumed.

Option 2: Trade sale to a strategic buyer

A trade sale to a competitor or adjacent business is often the highest-valuation exit available. Strategic buyers pay for synergies: your customer base, your team's expertise, your regional presence, your contracts. If there is a natural acquirer in your market who would benefit operationally from owning your business, the multiples can be attractive.

The trade-offs are real. Strategic acquirers typically have their own operational model, and yours gets absorbed into it. The brand may survive for a period as a commercial label while the back-office consolidates, or it may not survive at all. Key employees who were loyal to you personally often leave within 12 to 18 months of a strategic acquisition. The business you built continues to generate revenue for someone else, operating in ways that may have little to do with how you built it.

For founders whose primary goal is maximising the exit price and who have accepted that the business will change significantly afterward, a well-run trade sale is often the right answer. For founders who care about what happens to the team and the customers after they leave, the picture is more complicated.

Option 3: Traditional private equity

Private equity acquires businesses with a specific financial objective: buy, improve, and sell within a defined holding period, typically three to seven years. The sector has become more sophisticated about preserving operational culture, and there are funds that do this thoughtfully. But the structural incentives remain the same. The fund has a return target, a timeline, and investors to answer to.

For Belgian SMEs in the €1 to €5 million EBITDA range, traditional PE has a further complication: most funds of this type are not structured for businesses of this size. The economics of small transactions do not work at the typical buyout fund's fee structure. The firms that do operate in this range are often generalist or opportunistic, which means they are unlikely to know your sector well and unlikely to have a specific operational thesis for your business.

Private equity in Belgium has been active at the upper end of the mid-market. The lower end, where most Belgian SMEs actually sit, has historically been underserved by institutional capital with a genuine succession mandate.

Option 4: Management buyout

An MBO transfers ownership to the existing management team. If you have built a strong leadership layer and one or more of those people want to own the business, this can be a clean and culturally coherent solution. The people taking over already understand the operations. Customers and employees see continuity rather than change.

The constraint is almost always financing. Your management team is likely strong at running the business and unlikely to have significant personal capital to deploy. MBOs in this size range typically require external debt financing, and securing that financing depends on the strength of the business's cash flows and the bank's appetite for the deal. Management teams that have been operators their entire careers are often unfamiliar with the mechanics of deal financing, which means they need advisors, which adds cost and complexity.

MBOs are also emotionally complex. The people negotiating across the table from you are the people you have worked with for years. Getting the valuation right without damaging the relationship requires careful handling on both sides.

Option 5: Entrepreneurship through acquisition

Entrepreneurship through acquisition (ETA) is the mechanism through which an experienced external executive acquires and then leads an SME, typically with backing from an investment fund. It is a relatively young asset class in Europe, though it has been a recognised model in the United States since the 1980s.

The structure addresses several of the gaps in the other options. The buyer is a capable, motivated operator rather than a financial consolidator. The acquisition is the beginning of a long-term operating commitment, not a step toward a quick resale. And because the model is designed for businesses in the €1 to €5 million EBITDA range specifically, the economics work at this scale in ways that traditional PE typically cannot make viable.

According to the 2024 IESE International Search Fund Study, 79 percent of international search fund entrepreneurs had successfully acquired companies by the end of 2023, and the asset class has generated an overall ROI of 2.0x for investors. The Stanford GSB 2024 Search Fund Study, which tracks the US and Canadian market, recorded aggregate IRRs of 35.1 percent across all search funds as of December 31, 2023. These are not theoretical projections. They are returns from completed transactions.

What makes WAD Capital different from the other options

WAD Capital is a Belgian private equity firm structured specifically around the ETA model for European SMEs. Understanding what that means in practice starts with understanding the ownership structure: WAD holds 80 percent of each acquired business, and the incoming CEO earns a 20 percent equity stake, vested across value-creation milestones. This is not an absentee ownership model. The CEO is present, accountable, and financially motivated to build the business over the long term.

The firm operates within roughly 300 kilometres of Brussels, covering the Benelux and nearby regions. It targets businesses with €1 to €5 million in EBITDA, excludes distressed assets and loss-making companies, and focuses on operationally sound businesses where succession is the primary challenge rather than a fundamental business problem. If your company generates consistent cash flows, has a stable customer base, and needs new leadership rather than a turnaround, you are the profile WAD is designed for.

The comparison that matters most for most sellers is with the strategic buyer. Where a trade sale typically means absorption into a larger corporate structure, a WAD acquisition means your business continues operating as an independent entity under a new CEO who has been specifically selected for your sector and your context. The incoming operator is not managing your business as one of forty portfolio companies. They are running it as their business, with their own equity on the line.

Groupe Jordan, a Hainaut-based HVAC company acquired in October 2025, illustrates this in concrete terms. The founder, Jean-Luc Stavaux, reinvested following the acquisition and stayed on as Sales and Marketing Director. That is an unusual outcome in most exit structures. It happened because the transaction was designed around continuity rather than extraction.

WAD evaluates over 500 CEO candidates annually and selects approximately 10 per cohort. Each selected executive spends months developing a sector thesis and running diligence on targets through WAD's Deal Intelligence platform before any acquisition closes. The person who buys your business will have mapped your market carefully before your business appears on their list. They are not generalists looking for something to run.

For sellers, reinvestment is available in most cases. Some founders want a clean exit. Others want to remain involved as a minority shareholder without carrying the full operational load. WAD structures for both.

How a conversation with WAD works

First contact is confidential. If you are exploring whether a sale makes sense, what your business might be worth, and whether WAD's model fits your situation, a preliminary conversation carries no obligation and no formal process. The purpose is mutual understanding: WAD needs to understand whether your business fits the criteria, and you need to understand whether WAD's structure fits what you want from an exit.

Businesses that progress to a serious process will typically see an indicative valuation, a proposed deal structure, and an introduction to the CEO candidate who would lead the business. The process is designed to give you enough information to make a genuine decision before committing to anything.

If you have been building for thirty years and are starting to think about what comes next, the most useful thing you can do is start the conversation early, while you still have time to be selective about who takes over and on what terms.

Contact WAD Capital through wadcap.com to arrange a confidential discussion.