Why Some Founders Stay After Selling: The Case for Seller Reinvestment in SME Succession

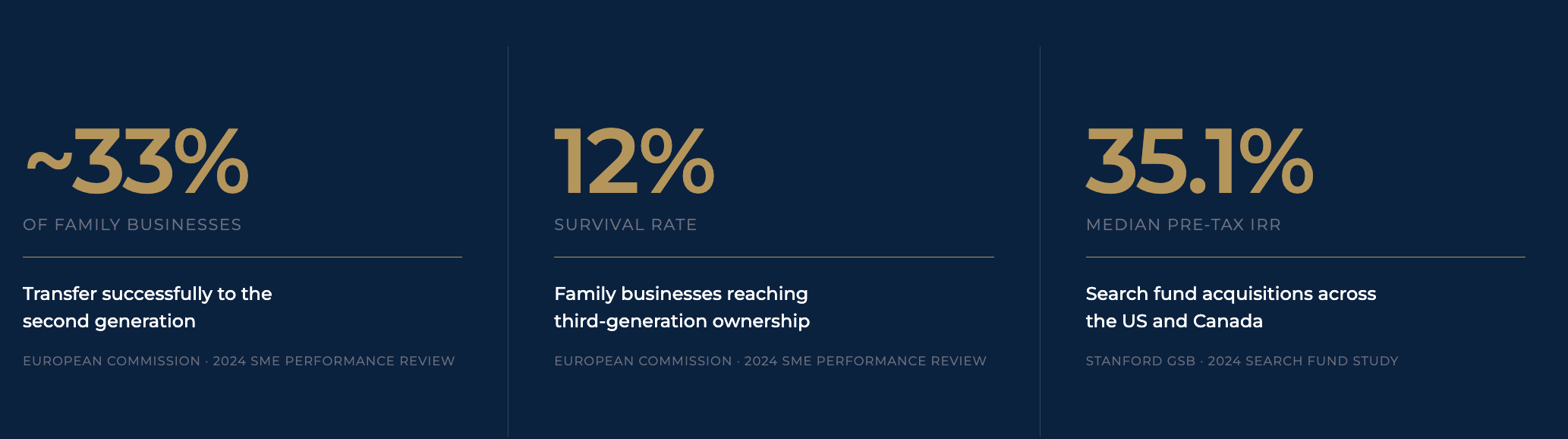

Some founders reinvest a portion of the sale proceeds back into the company they have just sold and continue working in a defined role. The structure is called seller reinvestment, and it is common in operator-led private equity acquisitions where continuity matters more than a clean exit. WAD Capital, a Belgian talent-driven private equity firm, allows retiring SME owners to reinvest up to 8% of the sale price alongside institutional capital. The selling founder keeps a financial stake in the next chapter of the business they built, while the incoming CEO takes operational control. According to the European Commission's 2024 SME Performance Review, only around a third of family businesses successfully transfer to the second generation, and roughly 12% survive to the third. Seller reinvestment offers a third path that most retiring founders do not know exists when they first start thinking about a sale.

What Is Seller Reinvestment in an SME Acquisition?

The mechanic is straightforward. When the business sells, the founder takes the bulk of the proceeds in cash and reinvests a defined percentage back into the new ownership structure. They become a minority shareholder alongside the institutional buyer and the incoming CEO. They keep a defined role inside the company, agreed before closing, with explicit scope and a fixed term.

The economics are not the headline. The alignment is.

A founder who has reinvested 8% of the sale price has an active stake in whether the business performs over the next five to seven years. They are not a former owner watching from the sidelines. They are a current shareholder with capital at risk. Their incentive to stay constructive after the handover is structural, not personal.

This matters because the alternative produces a known failure pattern. A founder who exits cleanly and walks away on the day of closing leaves behind a set of relationships that took thirty years to build and cannot be rebuilt in three months. Customers calibrated their loyalty to a specific person. Suppliers extended favourable terms based on a specific handshake. Employees followed a specific style of leadership. None of that is on the balance sheet, and none of it transfers automatically when the keys change hands.

Reinvestment buys the new owner time. It also buys the founder a continuing reason to care.

Why Would a Founder Want to Stay Involved After Selling?

The financial case is the easier one to explain. The harder one is the personal case, and it is the one that actually drives the decision.

Most founders who built a business over twenty or thirty years did not build it primarily for the eventual sale. They built it because they liked the work, the customers, and the team. Retirement from a business like that is not a single event. It is a transition that happens over years, and the question of what to do with the time, the network, and the operational knowledge does not have an obvious answer the day after closing.

A formal continuing role solves a real problem. The founder retains structure, a peer group inside the business, and the ability to contribute where their experience is genuinely useful. They give up the burden of being the final decision-maker on every operational question, which is the part most retiring founders are actually tired of, while keeping the parts of the work they still enjoy.

The financial logic is also stronger than it looks at first. A founder who sells outright at a fair multiple converts the business into a fixed sum, which then has to be reinvested somewhere. Public markets, real estate, other private companies. Each of those carries its own risk and provides no continuing connection to the founder's existing expertise. A reinvestment in the business they already understand, alongside an institutional fund and an incoming CEO who has been vetted over months rather than weeks, is often the highest-confidence allocation available to them.

The 2024 Stanford GSB Search Fund Study reports a median pre-money internal rate of return of 35.1% for search-fund acquisitions in the United States and Canada. Founders who reinvest at the close of an acquisition share in the value created during the hold period rather than walking away from it.

How Does the Dynamic Between the Incoming CEO and the Founder Actually Work?

This is the part most articles on succession leave out, and it is the part that determines whether the deal works in practice.

The dynamic is shaped by three things: scope, communication frequency, and clarity about who decides what. Each of them needs to be agreed before the founder formally steps into the new role, not negotiated as situations arise.

Scope. The founder's continuing role has to be specific enough to be operationally meaningful and narrow enough to leave room for the incoming CEO to lead. "Available for advice as needed" is not a role. "Sales and Marketing Director, focused on the top twenty customer accounts and the relationship with the regional supplier base, reporting to the CEO" is. The first arrangement creates ambiguity. The second creates accountability on both sides.

Communication frequency. The first 30 days of the post-acquisition period are governed in WAD Capital's programme by Step 12: Transition and Communication. During that window, the incoming CEO meets the founder weekly at minimum. Not as a status report. As a structured conversation about what the CEO is observing, what the founder thinks about it, and where the two views diverge. Some of the founder's observations will be operationally invaluable. Some will reflect how the business used to run rather than how it should run going forward. The CEO has to be able to tell the difference, and they cannot do that without consistent direct contact.

Decision rights. The single most important thing the founder and the new CEO agree on before day one is what happens when a long-standing supplier or employee bypasses the new structure and goes directly to the founder with a problem. It will happen. The founder needs to know whether to handle it, redirect it, or loop the CEO in. Without an agreed answer, every such call becomes a small test of authority that erodes the new CEO's position. With an agreed answer, the founder becomes part of the transition rather than an obstacle to it.

The tension nobody talks about openly is that the founder remains a gravitational field inside the organisation for as long as they are present. Employees who are uncertain about the new CEO will read the founder's body language for signals. Customers who built personal relationships will keep calling. Suppliers will defer to the founder's judgement. None of this is malicious. It is how trust works in businesses built on personal relationships. Managing it requires the founder to be visibly aligned with the new direction, which is significantly easier when they have capital invested in that direction succeeding.

Why Does Seller Reinvestment Work Better in Operator-Led Private Equity Than in Standard PE?

Standard private equity buys a company, installs financial discipline, optimises the capital structure, and exits within a defined window. The model works for businesses where the operational template is already understood and the value creation comes from leverage, multiple expansion, or a relatively standard set of efficiency improvements.

It does not work well for €1 to 5 million EBITDA SMEs where the founder still holds half the institutional knowledge in their head, the customer base depends on personal relationships, and the management team has never operated without the founder in the building. The reasons it does not work are the same reasons seller reinvestment is useful in the first place. The transition risk is concentrated in the human dimension, and a financial buyer is not structurally equipped to manage that risk.

Operator-led private equity changes the equation. The acquirer is a specific operator who has been selected, trained, and observed over months before the deal closes. They have a sector thesis they spent twelve months developing. They have an institutional fund behind them that provides 100% of acquisition financing, an investment committee that has assessed the deal, and a cohort of peers running parallel acquisitions whose collective experience compresses the operational learning curve. The founder is not selling to a fund. They are selling to a person, with a fund behind that person.

That structure is what makes seller reinvestment workable in practice. The founder reinvests because they have evaluated the specific human being who is going to run their business next, not because they trust an institution in the abstract. The 8% Seller Cap is not just a financial alignment device. It is a vote of confidence in the operator, made with capital rather than words.

What Does This Look Like in Practice?

Kaeron is the platform formed by WAD Capital's October 2025 acquisition of Groupe Jordan, a Hainaut-based HVAC business with around 110 employees. The incoming CEO isFrédéric Schilling, who spent the prior twelve months developing a thesis on the fragmented Belgian HVAC market and identified Groupe Jordan as the platform target before the deal was structured. The founder, Jean-Luc Stavaux, reinvested at closing and remained inside the business in a defined commercial role focused on customer and supplier relationships. Within three months, Kaeron completed its second acquisition, which built on the customer and supplier knowledge that came with the founding deal. The arrangement was not a condition imposed by either party. It was the structure that made operational sense for an HVAC platform whose growth thesis depended on continuity of the relationships the original founder had built over decades.

Is Seller Reinvestment Right for Every Founder?

No, and that matters.

Some founders genuinely want a clean break. They have spent thirty years inside the business, they have decided they are done, and the right outcome for them is a full exit and a different chapter. Asking those founders to stay involved produces friction, not value, and a structured acquisition without seller reinvestment is the better path.

Some businesses do not need it. A company with strong second-tier management already running operations, a customer base that buys on product rather than relationship, and a founder who has been deliberately stepping back over the prior two years can transition cleanly without continuing founder presence. Reinvestment in those cases is optional, not structural.

Where seller reinvestment becomes valuable is in the middle band: founders who care deeply about what happens next, businesses where institutional knowledge sits with the founder, and acquisitions where the incoming CEO needs eighteen months rather than three to absorb the operational reality of the company. That describes a meaningful share of European SME succession transactions in the €1 to 5 million EBITDA range. It is also the segment where most institutional capital does not operate, which is why most founders in this band are not offered the option in the first place.

The conversation worth having, before any of the structure is set, is the honest one about what the founder wants the next five years to look like. Reinvestment is a tool for a specific kind of transition, not a default setting. A buyer who proposes it without first understanding why it would or would not fit is not paying attention to the right question.

The CARE-PROFIT framework that governs WAD Capital's post-acquisition operations exists in part to make these arrangements legible to the founder before closing. What gets measured in the business after the handover. What the founder's continuing role actually consists of. How the new ownership structure handles the kinds of decisions that used to sit on the founder's desk. Most acquirers leave those questions vague until they cannot any longer. The point of getting them on paper before the deal closes is that the founder can then evaluate what staying involved actually means before deciding whether to do it.